Many options traders use the Double Calendar spread to profit from time decay and changes in volatility. But what if you could take that position, remove the risk, and still keep the profit potential? Here is the Double Calendar Time Machine.

Watch how Steve creates his risk-free Iron Condors

Steve Burnich

Steve Burnich is an options trader, educator, and founder of Navigation Trading. He has been trading since 1999 and has spent years developing and teaching options strategies focused on positive theta and risk management.

The idea behind the Double Calendar Spread Time Machine

Steve Burnich's strategy starts with a traditional double calendar spread. A Double Calendar combines two calendar spreads: a put calendar below the current price and a call calendar above it.

In a calendar spread, the trader sells a shorter-dated option and buys a longer-dated option at the same strike price. The position is entered for a debit and benefits from the relationship between the two option expirations.

The goal is not simply to hold the double calendar spread until expiration. Instead, Steve aims to generate a modest profit and then transform the position into a risk-free Iron Condor.

He calls this process the “DC Time Machine” because the strategy relies on time spreads and is designed to produce risk-free iron condors repeatedly.

- Other video interviews about calendar spreads

- Ravish Ahuja: Double Calendar Spread

- Vipul: Triple Calendar Spread

How the strategy works

The first step is opening a Double Calendar spread. Steve primarily trades SPX and typically chooses strikes around the 30 to 40 delta range on both sides of the market.

His preferred setup uses options in the following week's expiration cycle. The short options are often six to fifteen days from expiration, while the long options are usually only one to four days further out.

After entering the position, he watches for a relatively small profit. Depending on the exact structure, this is often in the range of 5% to 10%.

Once enough profit has accumulated, he enters what he calls a transformer order.

The transformer order closes the longer-dated options and simultaneously purchases the wings needed to create an Iron Condor using the remaining short options.

If the credit received from the transformation is large enough, the resulting iron condor becomes risk-free.

Steve aims to be able to transform the Double Calendar spread within the first day. If that is not possible, he will usually choose to close the trade at the end of the day.

The key requirement for a risk-free Iron Condor

According to Steve, the transformation only works when the credit received exceeds the original debit by at least the width of the iron condor wings.

For example, if a trader paid $10.10 for the original double calendar spread and wants to create an iron condor with five-point-wide wings, the transformation must generate at least $15.10 in total credit.

At that point, the maximum possible loss is eliminated.

Any additional credit collected beyond that level increases the minimum profit of the position.

Why volatility matters

A major part of the strategy revolves around implied volatility.

Steve explains that the relationship between the implied volatility of the short options and the long options is more important than the absolute volatility level itself.

The ideal situation is for the front-month implied volatility to contract faster than the back-month implied volatility after the trade is entered.

When that happens, the double calendar spread tends to gain value.

To help identify favorable conditions, Steve developed a proprietary tool called Flux. The software tracks the relationship between front and back implied volatility across different expiration cycles and helps provide context for potential entries.

He stresses that the tool is not predictive. Instead, it helps traders understand current market conditions and identify situations where mean reversion in volatility may work in their favor.

Managing risk before and after transformation

One of the most important points Steve makes is that the strategy is not risk-free when it begins.

The risk exists while the position is still a double calendar spread.

If the market makes a large move before the transformation occurs, losses can develop. For that reason, he emphasizes position sizing and personal risk tolerance.

His general rule is to exit if losses reach approximately 20% of the original double calendar position.

Once the transformation has been completed, however, the management becomes much simpler.

Because Steve primarily trades SPX, which settles in cash, he does not need to worry about assignment. After transformation, many positions can simply be held until expiration.

Recycling buying power

One of the concepts Steve believes traders often overlook is buying power efficiency.

When the double calendar spread is transformed into a risk-free iron condor, the broker no longer requires buying power for the original risk.

That capital can then be deployed into new trades while the transformed position remains open.

Steve refers to this as recycling buying power and considers it one of the most powerful aspects of the strategy.

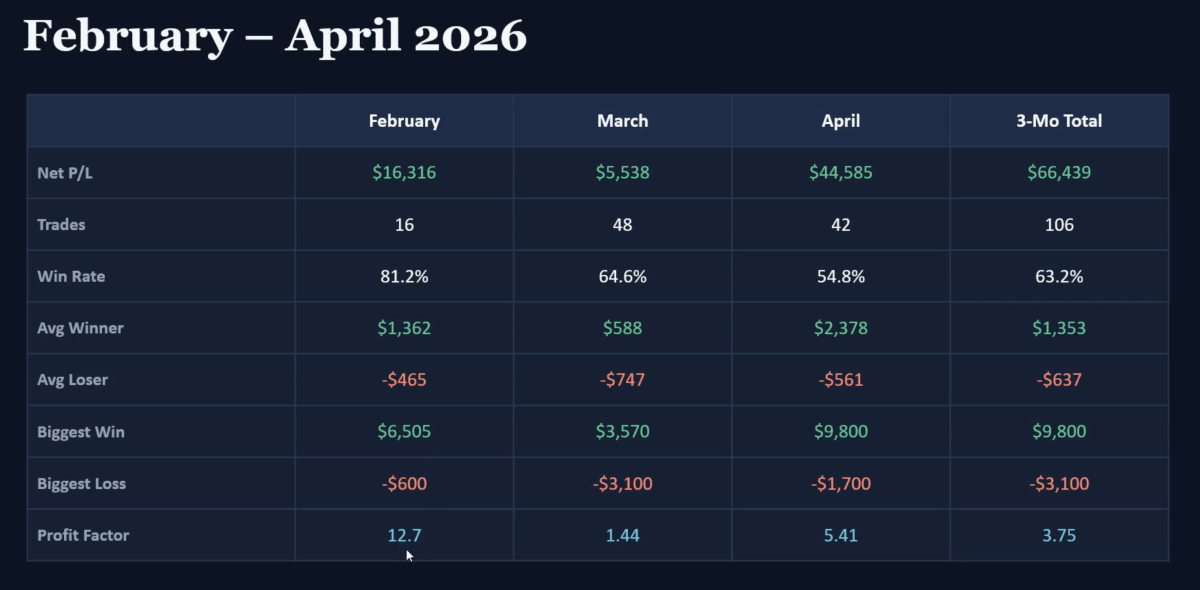

Results and risk profile

Steve estimates that approximately 60% of his double calendar spread trades are transformed into risk-free structures within the same day or the following day.

On a risk scale from one to ten, he rates the initial double calendar spread as roughly a three or four because of its relatively wide profit zone and defined-risk nature.

Once transformed, he considers the position effectively risk-free.

For traders interested in advanced options strategies, the DC Time Machine offers an intriguing variation on the traditional double calendar spread. By focusing on volatility relationships, careful trade construction, and capital efficiency, Steve has developed a method designed to remove risk while preserving the opportunity for substantial profits.

📚 Books recommended in this video

Steve recommends these three books:

- Mark Douglas: Trading in the Zone

- Jared Tendler: The Mental Game of Trading

- James Clear: Atomic Habits

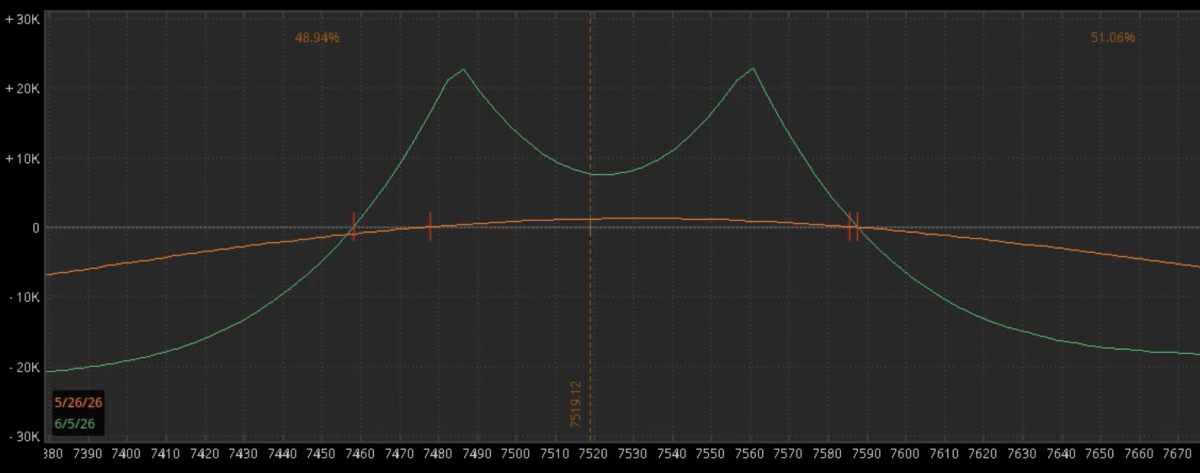

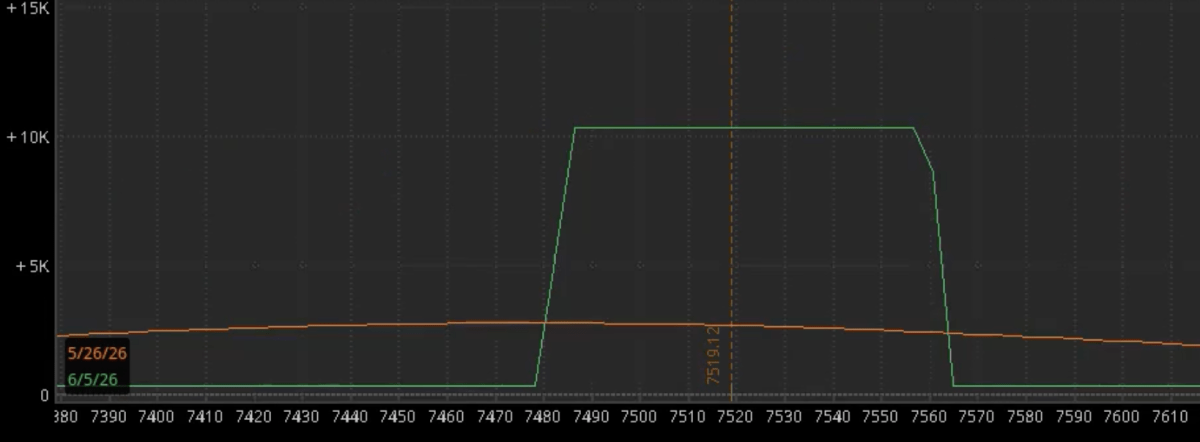

I was trying to reconstruct the example above, it seems the transformation happened on 5/26 at 8 DTE, with 30 or so delta it seems max profit and loss of the iron condor would be roughly 1:1. If this observation is correct, you’d have $2.5 profit on the double calendar (or 25%), so why wouldn’t you simply close the DC for a nice profit? How is the IC improving your P&L? Maybe I am missing something, would you mind share some exact contract data of the trade to help me better understand?

My question exactly, I have transformed 2 Double Calendar Spreads this way and still have no idea how it helps and why you wouln’t just close the spread for a profit and move on. Maybe I am dense but if you ever figure it out, let me know. It basically (at least in ToS, converts them into a Debit Strangle and a Credit Strangle if you combine them you get an IC. Still not sure why you would do this, but I am sure there is some super secret traders formula that explains it.

[…] Steve Burnich: Double Calendar Time Machine […]