- This article and video have been produced in cooperation with Option Omega. Theta Profits has an affiliate relationship with Option Omega, and may earn a commission if you sign up through our link.

Many options traders spend hours backtesting strategies, only to discover that their live results look nothing like their historical tests. In this interview, Matt Simon, co-founder of Option Omega, explains why that happens and shares three common backtesting mistakes that can lead traders astray.

Learn about three common backtesting mistakes

Why backtesting matters

Backtesting is the process of testing a trading strategy on historical market data. The goal is not to prove that a strategy worked in the past. The goal is to determine whether the strategy is robust enough to have a reasonable chance of working in the future.

According to Simon, a backtest should help traders build confidence by showing how a strategy would have performed across different market environments, volatility regimes, and economic conditions. However, that confidence is only justified if the backtest reflects reality.

Over the years, Simon has talked to thousands of options traders about how they backtest their options strategies. He has identified three common mistakes traders often do when backtesting.

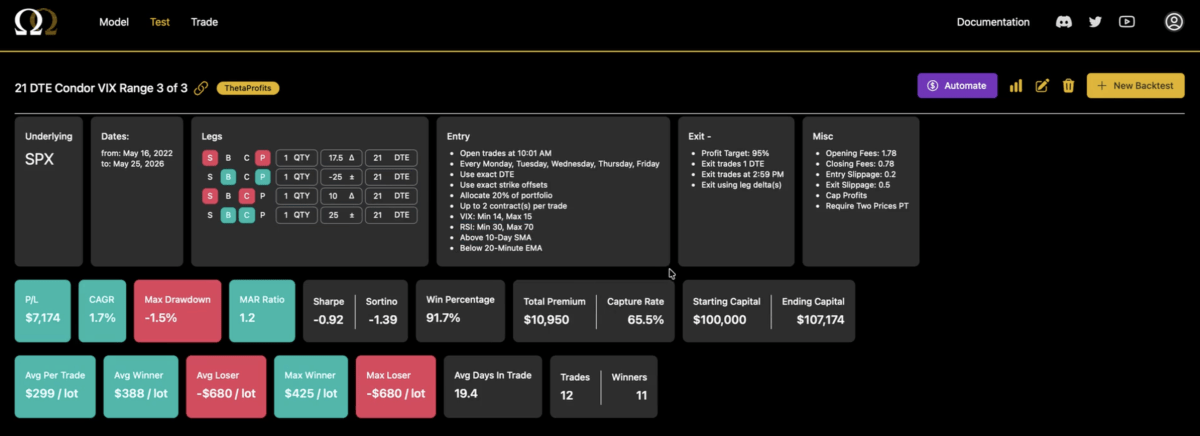

Option Omega

…is a platform for backtesting, automation and trade modelling. With Option Omega you can backtest your options strategy with data going back to 2013. Once you have identified your strategy, it can easily be automated. Option Omega also has a powerful tool to model your trades.

Get 50% OFF your first year with Option Omega with this affiliate link

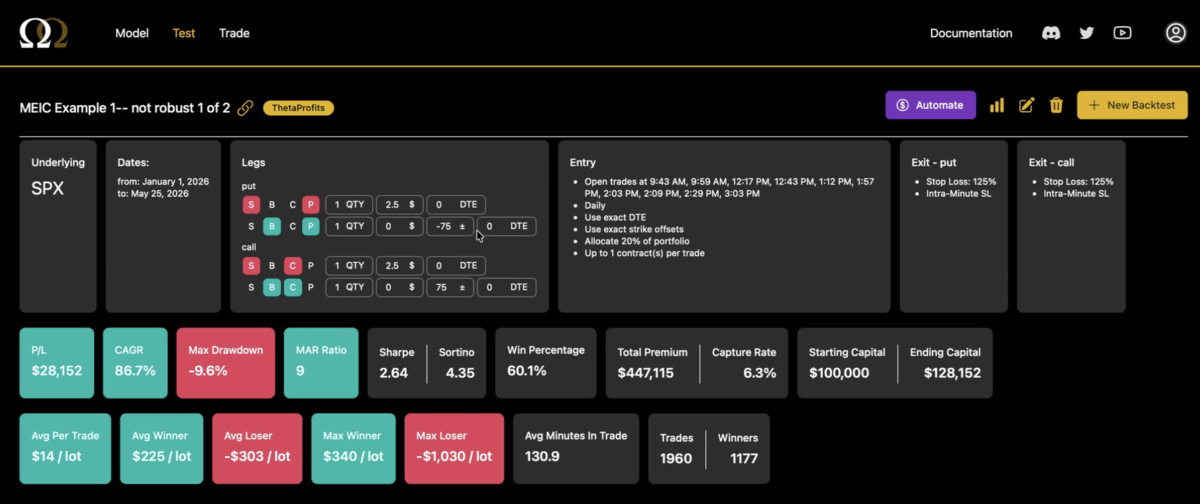

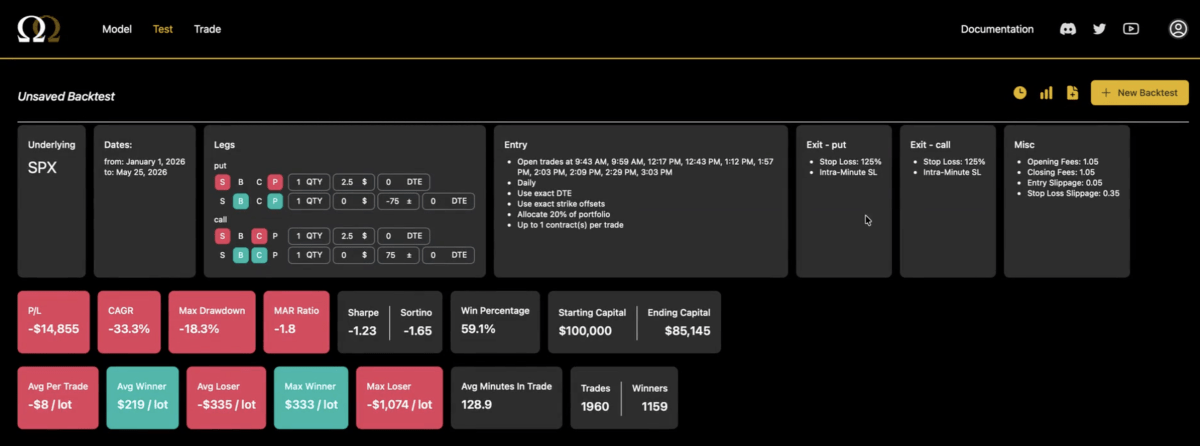

Mistake #1: Building an unrealistic backtest

The first and most common mistake is failing to make the backtest realistic.

Simon demonstrates how a strategy can appear highly profitable when tested using ideal assumptions. But when realistic costs such as commissions, fees, and slippage are added, the same strategy may become unprofitable.

Slippage is particularly important in options trading. Most backtesting platforms use historical mid-prices as a reference point. In reality, traders are often filled away from the midpoint, especially when entering or exiting positions under pressure.

Ignoring these costs can dramatically distort the results.

The takeaway is simple: a backtest should be as close to real-world trading conditions as possible. Traders should account for opening and closing costs, realistic fills, and any other factors that may impact actual performance.

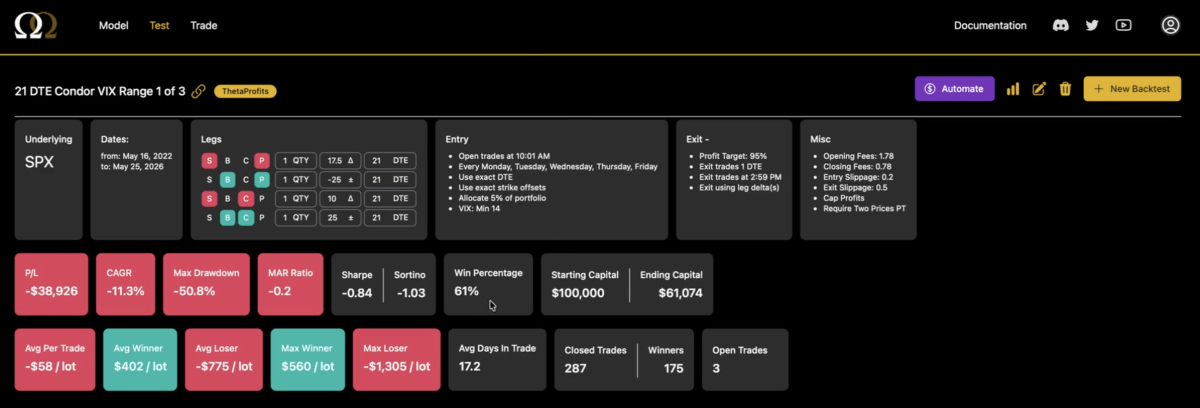

Mistake #2: Overfitting the strategy

The second mistake is overfitting.

Overfitting occurs when traders continuously tweak filters and parameters until the backtest produces attractive results. Examples include narrowing volatility ranges, adding multiple technical indicators, or adjusting entry criteria to remove losing trades from the historical record.

At first glance, the results may look impressive. Win rates improve, drawdowns shrink, and performance metrics become more attractive.

The problem is that the strategy often becomes so specific to historical conditions that it loses its ability to perform in the future.

Simon describes this process as “polishing dirt.” Instead of creating a genuinely robust strategy, traders are simply finding ways to make the historical data look better.

A good backtest should not depend on extremely precise values or highly restrictive filters. If small changes in the inputs dramatically change the results, that may be a warning sign that the strategy has been over-optimized.

Mistake #3: Trading without a clear thesis

The third mistake is backtesting and trading strategies without understanding why they work.

With modern tools, traders can generate ideas, backtest them, and even automate them faster than ever before. Artificial intelligence and automated strategy builders have made the process easier and more accessible.

But Simon warns that convenience can create a new problem.

Many traders backtest and deploy strategies they do not fully understand. They may know the rules, but they cannot explain the underlying logic or edge.

That becomes dangerous when markets behave unexpectedly.

Options are leveraged instruments, and traders who do not understand their positions may struggle to react appropriately during periods of high volatility or sudden market moves.

Before trading a strategy, traders should be able to clearly explain why they believe it has an edge and under what conditions it is expected to perform well.

What successful backtesters do differently

Simon also highlights several practices used by the most successful members of the Option Omega community.

The first is that they can clearly articulate their thesis. They know why they are testing a strategy and what market behavior they expect to exploit.

The second is that they seek feedback from other experienced traders.

Rather than working in isolation, they share ideas, discuss assumptions, and challenge their conclusions. This process often reveals weaknesses that may not be obvious when working alone.

Finally, successful traders treat backtesting as part of a broader learning process. They use historical testing to build understanding, not simply to find attractive statistics.

- You may also watch our interview with Tammy Chambless: Backtesting options strategies made easy.

Key takeaways on backtesting

Backtesting is one of the most valuable tools available to options traders, but only when used correctly.

Matt Simon's three main lessons are:

- Make your backtests realistic by including slippage, fees, and other real-world costs.

- Avoid overfitting by resisting the urge to endlessly tweak parameters.

- Never trade a strategy unless you understand the thesis behind it.

The goal of backtesting is not to create the most impressive historical performance report. The goal is to develop a strategy that you can confidently trade in the real world.

A robust backtest may not look perfect, but it is far more valuable than one that does.

Totally agree on the backtest trap — I see it all the time with gold strategies that look perfect in history but blow up on live data. The real killer is overfitting to calm market conditions and then getting wrecked during geopolitical spikes or NFP. I actually used Ratio X EA Generator to build a custom XAUUSD EA that bakes in session-specific logic and wider spreads during news, since generic builders miss how gold behaves under stress. Took a couple iterations and some credits to dial in the parameters, but it’s way better than trusting some one-size-fits-all template. Have you found backtesting tools that actually account for volatility regime changes, or do you still validate everything on live micro accounts first?