The trades of my interview guest, Vipul, show an average return of about 6.33% over 11 days, offering a benchmark for how the triple calendar can perform when traded with discipline.

Learn how Vipul trades triple calendar

Who is Vipul?

Vipul is a retail options trader who began his trading journey in the United States in 2019. After experimenting with different strategies and struggling with directional trading, he shifted his focus to calendar spreads. Today, he is based in New Delhi, India, where he continues to refine and trade his triple calendar strategy as his primary approach.

The triple calendar spread

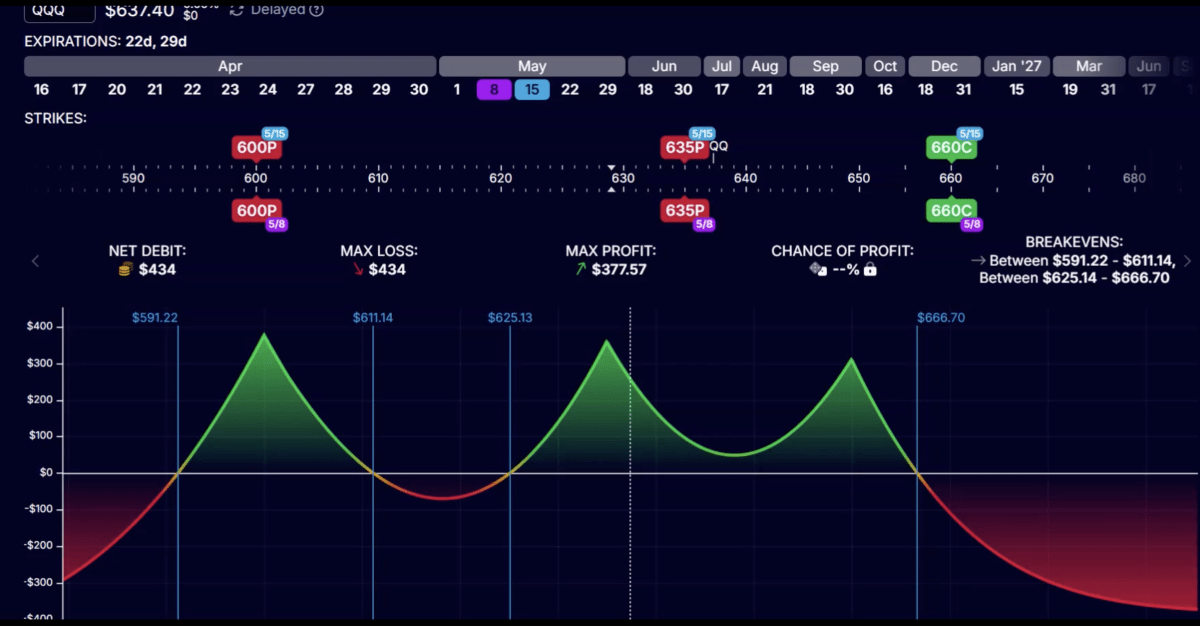

A triple calendar is a combination of three calendar spreads. A standard calendar spread involves selling a near-term option and buying a longer-term option at the same strike price.

In the triple calendar setup, Vipul places:

- One calendar at the money

- One calendar above the current price

- One calendar below the current price

This creates a payoff structure that allows the trade to perform across a wider range of price movements.

- Watch other interviews on Theta Profits:

- Ravish Ahuja: Double Calendar spread

- Simon Black: The Time Flies Spread

- Steve Ganz: Butterfly options trades explained

The triple calendar in different market conditions

The core idea behind the triple calendar options strategy is to reduce reliance on market direction. By spreading the position across three strike areas, the strategy can adapt to different scenarios.

If the market:

- Moves up → the upper calendar gains value

- Moves down → the lower calendar benefits

- Moves sideways → the at-the-money calendar performs best

This makes the triple calendar attractive for traders who find it difficult to consistently predict direction.

How Vipul selects strikes

Strike selection is a key part of the strategy. Vipul uses the expected move – derived from the straddle price- to determine where to place the upper and lower calendars.

His process:

- Identify the at-the-money strike

- Calculate the expected move using the straddle price

- Place the upper and lower calendars around that range

- Adjust slightly based on support and resistance levels

This helps create a balanced position with enough room for the trade to develop.

Expiration setup

Vipul uses a consistent structure for expirations:

- Sell options around 21 days to expiry (DTE)

- Buy options with around 28 days to expiry

This one-week difference forms each calendar spread. Trades are typically aligned with weekly expirations.

Entry timing and conditions

The triple calendar is designed as a repeatable strategy. Vipul often enters a new trade shortly after exiting the previous one.

However, he avoids entering trades around major events such as:

- FOMC meetings

- CPI releases

Instead, he prefers setups where such events fall between the short and long legs.

Profit target and exit rules

Discipline is central to the strategy.

- Profit target: Around 10% of the initial debit

- Typical duration: 2 to 10 days

- Hard exit: Close the trade when 7 days remain to the expiry of the short leg, no matter what the profit or loss is at that time.

By exiting early, Vipul avoids the increased volatility and risk that often occur in the final week before expiration.

Managing risk and adjustments

While the triple calendar is more stable than many directional strategies, adjustments are sometimes needed.

If the underlying moves beyond the upper or lower range, Vipul may:

- Add another calendar further out in the direction of the move

This helps rebalance the position and maintain exposure across price ranges.

He typically keeps existing calendars open rather than closing them early, as they may recover if the market reverses.

The biggest risk: A drop in volatility

One of the biggest risks with the triple calendar strategy is a sustained drop in volatility. Since calendar spreads are positive Vega trades, they generally benefit when implied volatility rises. If the volatility declines while the underlying price also moves slowly or stays within a narrow range, the position may take longer to become profitable or fail to reach the target before the planned exit.

In these situations, the trade can stagnate, and time decay from the short leg may not be enough to offset the loss in volatility, making patience and strict exit rules especially important.

Performance and expectations

Based on Vipul’s shared data from 2025:

- Win rate is around 80%

- Average return was 6.33% per trade

- The average duration was about 11 days

Losses do occur and can be larger than gains in some cases, but the strategy relies on consistency over time.

A strategy built on consistency

The triple calendar is not about large, one-off wins. Instead, it focuses on:

- High-probability setups

- Small, repeatable gains

- Structured risk management

For traders seeking a more systematic approach, Vipul says it offers a way to participate in the market without relying heavily on directional forecasts.

is expected move based on todays straddle or 21 day straddle?

In the video he explains that he bases the expected move on the straddle price of the date the shorts expire, so the 21-day straddle.

Hi John, Vipul – the bid ask spread on options that far out in terms of both time and money is pretty big. The more legs you add the more the spread widens. Curious how you handle that?

Are all spreads Call spreads or Put spreads or both?

[…] Vipul: Triple Calendar Spread […]