Time Flies is an advanced delta-neutral options strategy designed to profit from theta decay while handling changes in market volatility. In this interview, Simon Black explains how he builds the trade using diagonals and broken-wing butterflies, why he focuses on creating the “perfect curve,” how he manages risk and makes adjustments, and how the strategy has performed over three years of live trading.

Learn about the Time Flies strategy

Simon Black

Simon Black is a New Zealand-based options trader with an engineering background who specializes in designing and refining options strategies. He publishes his trades and results publicly and has now traded the Time Flies strategy consistently for three years.

What is the Time Flies strategy?

The Time Flies strategy combines two separate option structures:

- A put diagonal below the market

- A call broken-wing butterfly above the market

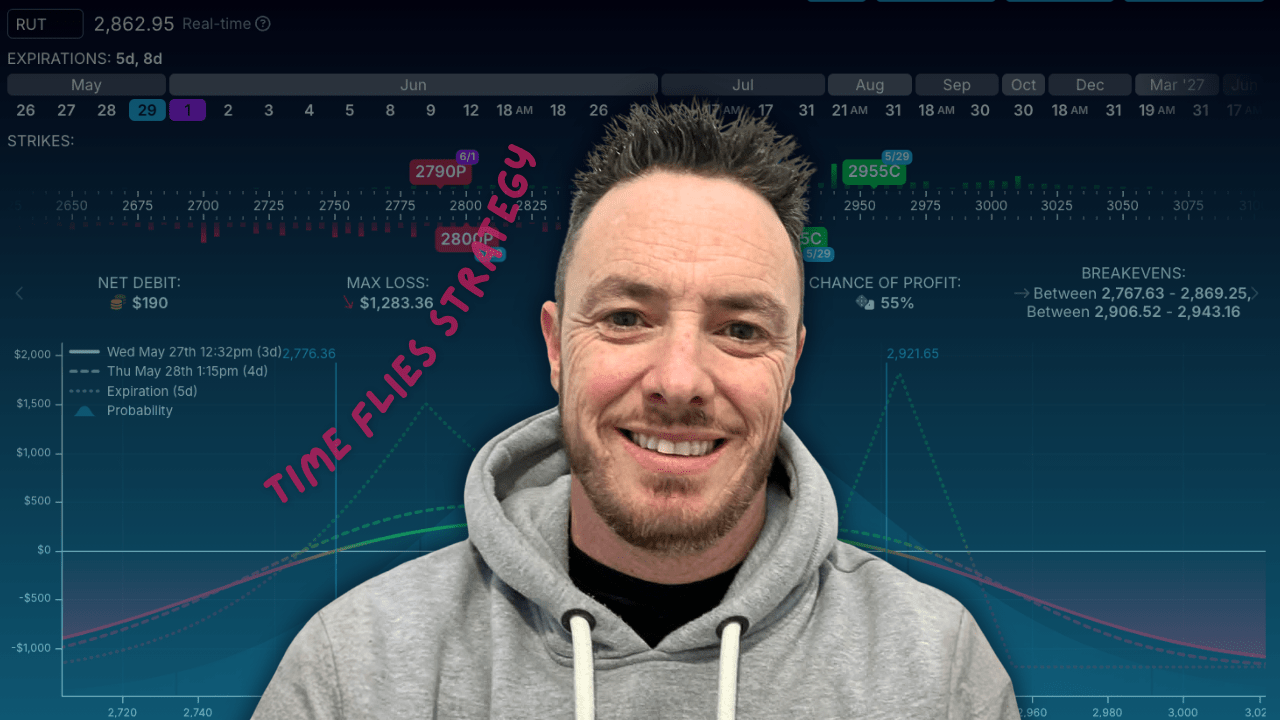

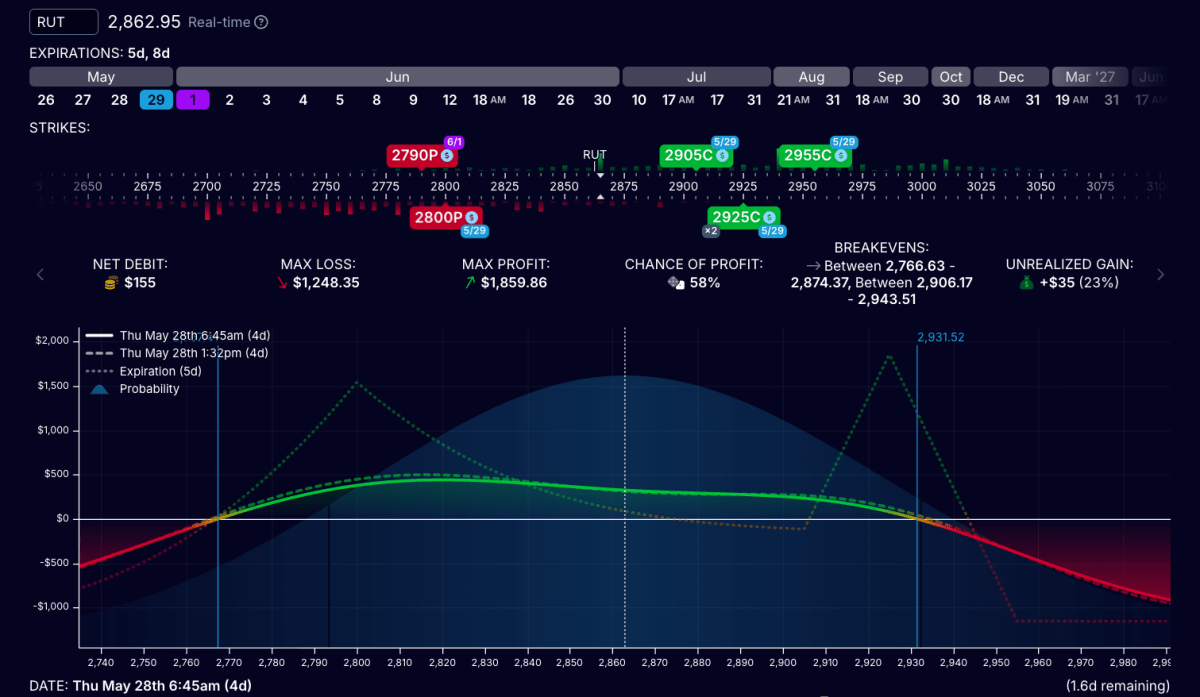

The goal is to create a balanced profit curve that can benefit from time decay while still tolerating normal market movement. Simon repeatedly emphasizes that creating the right curve is the key to the strategy.

Simon opens the trades on Thursdays, with the call broken-wing butterfly and the short in the diagonal expiring on Friday the week after, and the long the following Monday.

Unlike directional trading strategies, Time Flies is designed to remain largely delta-neutral. Simon explained that he stopped trying to predict market direction long ago and instead focuses on creating trades that can perform if the market stays relatively stable.

- Relevant videos to watch

- Steve Ganz: The Flyagonal strategy (similar to Time Flies)

- Steve Ganz: The Flydagonal strategy

- Ravish Ahuja: Double Calendars

Why volatility matters

A major part of the strategy is how it reacts to changes in implied volatility.

The put diagonal below the market tends to benefit when volatility rises during market declines. Meanwhile, the broken-wing butterfly above the market can benefit when volatility contracts during market rallies.

According to Simon, this relationship makes index products particularly suitable for the strategy. He mainly trades Russell 2000, but has also used SPX, QQQ, and futures options.

He explained that he eventually preferred Russell because it allowed him to build wider and smoother curves than SPX did.

Building the “perfect curve”

One of the most interesting parts of the interview is Simon’s explanation of how he constructs the trade each week.

He does not use a rigid formula or fixed delta system. Instead, he manually adjusts strikes and widths based on current volatility and market conditions.

When volatility is low, he places strikes closer to the market. When volatility rises, he can move them further away while still maintaining a balanced trade structure.

Simon described the process almost as artistic. Using OptionStrat, he visually shapes the trade until the curve looks smooth and balanced without large weak spots. Also the two profit tents should be at about the same height.

According to him, the quality of the curve is more important than any single rule or setup formula.

Profit targets and exits

Simon uses buying power as the main reference point for his risk and profit targets.

He aims for profits around 10% of buying power and will exit once that target is reached. He explained that over time, he has become increasingly willing to “take the money and run” instead of holding for maximum gains.

One of his strictest rules is avoiding the final day before expiration. He will always be out of the trade at least 24 hours before the closest expiry date.

As expiration approaches, the shape of the profit curve changes rapidly and becomes much more sensitive to price movement and volatility changes. A trade that looks excellent one day can quickly turn into a loss during the final trading session.

How he adjusts trades

Although most trades are not adjusted, Simon also explained how he manages positions when the market moves aggressively.

For downside adjustments, he often uses calendars because they can expand the downside portion of the curve and benefit from volatility increases.

For upside moves, he may use call calendars or diagonals to create a new upside target area.

However, he stressed that adjustments are mainly defensive. The goal is typically to reduce damage or recover part of the position rather than create a large winning trade from a bad situation.

He also emphasized that small losses are a completely normal part of trading and should not be feared.

The results so far

The strategy has attracted significant attention because Simon publishes his results weekly.

- Results in 2024: 45.2% annualized (he started trading in September)

- Results in 2025: 100.3%

- Results in 2026: 41.0% as of May 24 (104.6% annualized)

Simon measures his results as a percentage of the capital he has allocated to the strategy. He allocates $3,000 per contract for trades in RUT, although he will typically only use $1,200 in buying power per trade.

Theta Profits host John Einar Sandvand also shared his own experience trading Time Flies with SPX.

His results after one year of trading:

- 57 trades – 46 winners

- Average net profit of 5.33% per trade. This is measured against the used buying power.

- The average trade lasted 5.7 days.

📚 Books recommended in this video

Here are three books that Simon recommends options traders to read:

- Nassim Nicholas Taleb: Fooled by Randomness

- Mark Douglas: Trading in the Zone

- Julia Spina: The Unlucky Investor’s Guide to Options Trading

[…] Simon Black: Time Flies strategy […]