Short strangles are among the most popular premium-selling strategies in options trading. In this interview, German trader Reiner Hofmann explains how he uses a rules-based short strangle strategy on the Russell 2000 Index (RUT), including his entry criteria, adjustment methods, and risk controls. After three years of trading the strategy, he has yet to experience a loss.

Learn Reiner's RUT short strangle strategy in this video

Reiner Hofmann

Reiner Hofmann is a former executive in the technology industry who now focuses full-time on options trading. Over the past several years, he has worked closely with a professional coach and developed a structured approach to volatility-based trading. He lives in Hammelburg in North Bavaria in Germany. Together with Professor Kai Oberländer, he has recently launched the options trading platform Edgeseeker in the German market.

What is a short strangle?

A short strangle consists of selling an out-of-the-money put and an out-of-the-money call on the same underlying and with the same expiration date.

The trader collects premiums from both options and profits if the underlying remains within a certain range. Unlike an iron condor, a short strangle does not include long protective options. As a result, it generates more premium and more theta decay, but it also carries theoretically unlimited risk.

According to Hofmann, the strategy is not primarily a directional bet.

Instead, he views it as a way to sell time and volatility.

As he explains in the interview, options are often influenced more by the expected magnitude of future movement than by direction itself. His goal is to profit when the market moves less than what the options market has priced in.

- Watch some of our other interviews:

- Boomer Dan: Burrito Butterflies

- Steve Burnich: Double Calendar Time Machine

- Simon Black: Time Flies strategy

Why Reiner Uses the Russell 2000

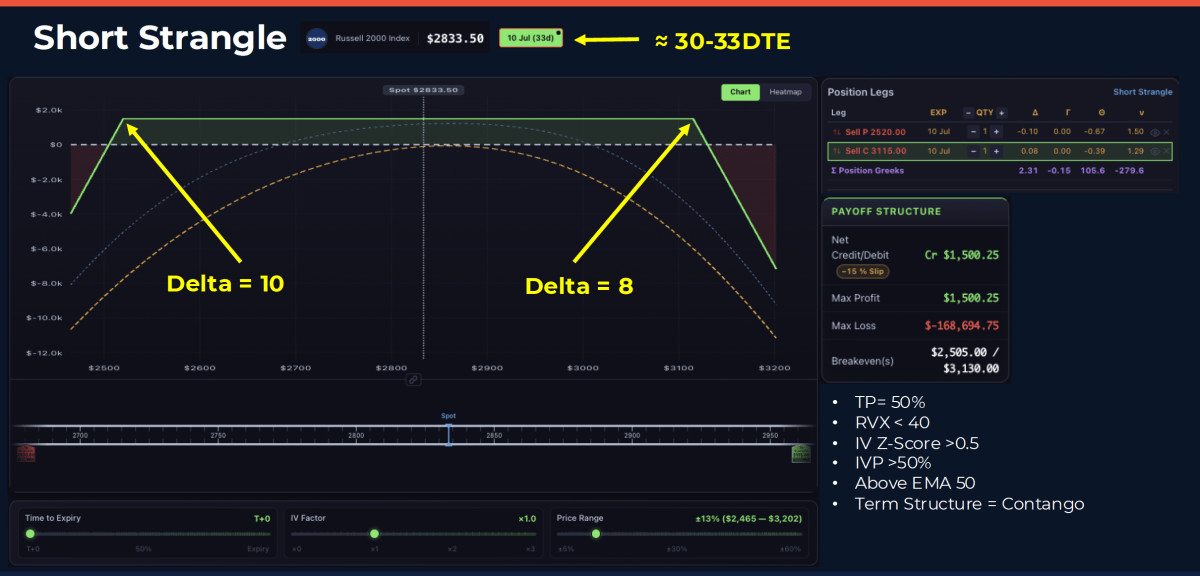

Hofmann's primary income-oriented short strangle strategy is traded on the Russell 2000 Index (RUT).

After extensive testing, he found that a 30-day-to-expiration setup provided the most attractive balance between premium collection and risk.

His standard structure consists of:

- Short 10-delta put

- Short 8-delta call

- Approximately 30 days to expiration

- 50% profit target

He emphasizes that the 50% profit target is critical. Rather than holding positions until expiration, he prefers to exit early and avoid the increasing gamma risk that develops as expiration approaches.

The average holding period is approximately 14 days.

The entry criteria for the RUT short strangle

One of the most valuable parts of the interview is Hofmann's detailed explanation of his entry filters.

He does not sell short strangles simply because the premium appears attractive.

Several conditions must be present before he enters a trade.

First, implied volatility should be elevated relative to realized volatility. He uses either the IV Z-score or the IV percentile to evaluate whether options are sufficiently expensive.

Second, the volatility environment should not reflect excessive market stress. For RUT, he prefers the RVX volatility index (similar to VIX, but for RUT) to remain below 40.

Third, the term structure should be in contango.

This is a key concept in Hofmann's process. When volatility futures are in contango, future volatility is priced higher than current volatility. As time passes, he benefits not only from theta decay but also from the tendency of volatility to roll down the term structure.

Finally, he prefers a market that is not strongly trending in either direction. He often uses indicators such as RSI to help identify a more neutral environment.

How he manages risk

Reiner argues that risk management is where most of the edge in the strategy comes from.

His first adjustment trigger occurs when either short option reaches approximately 35 delta.

At that point, he evaluates the market environment and decides whether adjustments are necessary.

Possible actions include:

- Closing the threatened side

- Rolling the untested side closer to the money to collect additional premium

- Rolling positions to a later expiration cycle

- Re-centering the position to reduce directional exposure

A key rule is that adjustments should be executed for a credit whenever possible.

Hofmann also maintains a hard loss limit. If losses reach approximately 20% of the margin required for the position, he exits the threatened side.

This creates a predefined risk-management framework despite the strategy's theoretically unlimited risk profile.

But throughout the interview, he underlines that this is a strategy with unlimited risk, and thus it is not suitable for a beginner trader.

Hedging the tail risk

Because short strangles carry undefined risk, Hofmann also discusses several hedging methods.

One approach involves using Russell futures as an emergency hedge if the underlying reaches predefined trigger levels.

Another approach is purchasing a long strangle against the short strangle. This creates a defined-risk structure that can help protect against large market moves.

He also notes that traders can always convert a short strangle into an iron condor by purchasing protective wings if market conditions change.

Results of trading short strangle

Hofmann tracks all of his trades in a simple spreadsheet and evaluates performance based on the capital allocated to the strategy.

Over the past three years, he reports an average annual return of approximately 25% on the portion of his portfolio dedicated to these trades. Despite those results, he describes himself as a conservative and risk-averse trader. His personal target is only 10% per year, viewing anything above that as a bonus.

He credits the performance not to aggressive position sizing, but to disciplined risk management, careful trade selection, and strict adherence to predefined rules. According to Hofmann, position sizing is one of the most important factors behind long-term success with a short strangle strategy.

He places around 25 trades a year and says he has, so far, after three years, yet to experience a loss.

📚 Books recommended in this video

Reiner Hofmann recommends these three books to learn about options trading:

- Charles M. Cottle: Options: Perception and Deception

- Sheldon Natenberg: Option Volatility & Pricing

- Lawrence G. McMillan: Options as a Strategic Investment