Most options traders spend years searching for the next great strategy. In this interview, Roman argues they're looking in the wrong place. Instead of chasing new trade setups, he believes traders should focus on building a balanced portfolio where individual strategies become tools rather than the source of their edge.

Learn how Roman builds a market-neutral options portfolio

Trader from Poland

Roman is a quantitative trader, former hedge fund manager, and founder of Options Jive. He is originally from Krakow in Poland, but now lives in Dubai.

With nearly 20 years of options trading experience, he focuses on teaching traders how to build market-neutral portfolios that aim to generate consistent income from time decay instead of relying on market direction.

Stop looking for the perfect strategy

The central message of this interview challenges one of the most common beliefs among options traders.

Many traders spend years searching for better strategies – iron condors, butterflies, calendar spreads, strangles, or the latest “shiny object.” Roman believes that search is largely misguided.

According to him, individual strategies are not where your long-term edge comes from. Instead, consistent results come from how your trades work together inside a portfolio.

Rather than asking, “Which strategy should I trade next?”, Roman asks a different question:

“What does my portfolio need?”

That shift in thinking forms the foundation of his entire trading approach.

A different way to think about options

Roman's goal is to build a market-neutral options portfolio.

Instead of trying to predict whether the market will rise or fall, he attempts to remove as much directional exposure as possible. His objective is to let theta decay become the primary source of returns.

His philosophy is based on a simple observation.

Even after nearly 20 years in quantitative finance, he says he cannot consistently predict market direction. Rather than spending energy on something he cannot control, he prefers to focus on the variables he can control: portfolio exposure, buying power, theta generation, and risk management.

The result is a portfolio designed to perform regardless of whether the market moves up or down.

Why beta-weighted delta matters

One of the key concepts throughout the interview is beta-weighted delta.

Unlike ordinary delta, beta-weighted delta measures the entire portfolio's exposure to market movements by adjusting each position according to the volatility of its underlying asset.

Instead of looking at dozens of individual positions, traders can monitor one single number that reflects the portfolio's overall sensitivity to moves in the S&P 500.

Roman aims to keep that number as close to zero as possible.

Whenever the portfolio becomes too bullish or too bearish, he adjusts positions until the portfolio returns to a market-neutral state.

He argues that beta-weighted delta is one of the most valuable metrics available on modern broker platforms, yet many traders never even look at it.

Building the portfolio

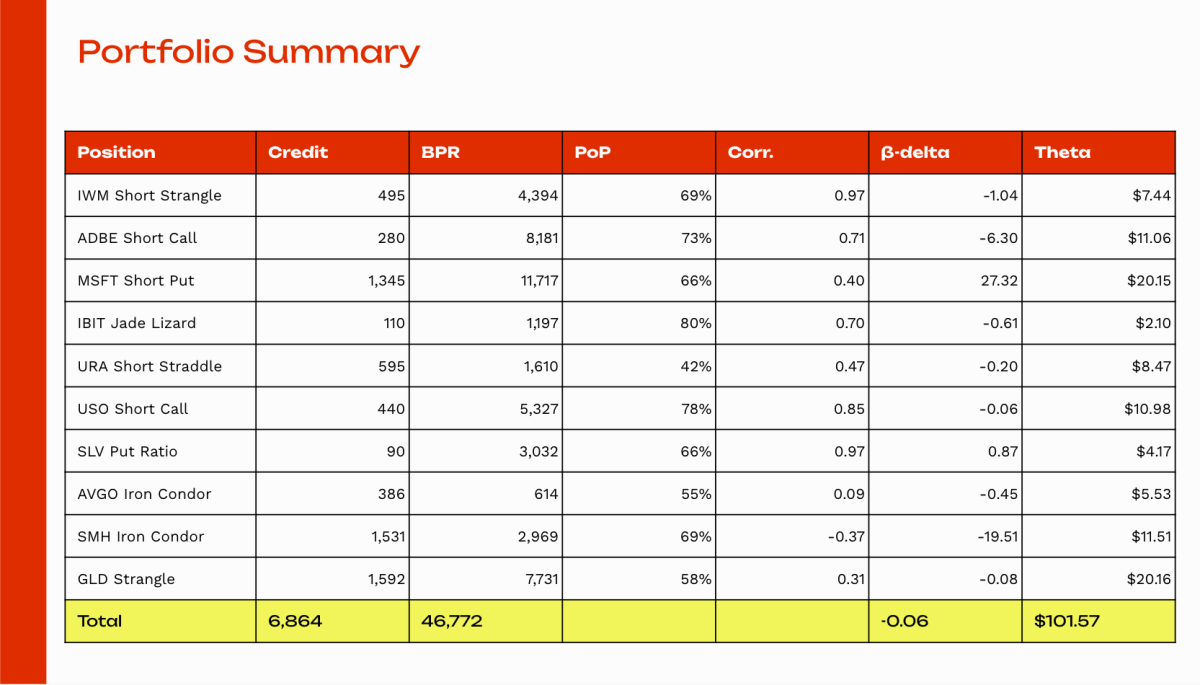

To demonstrate the concept, Roman constructs an example portfolio for a $50,000 account.

Instead of relying on one favorite strategy, he combines a wide variety of premium-selling trades across different markets.

His example includes positions in broad market ETFs, technology stocks, commodities, precious metals, energy and cryptocurrencies.

The portfolio uses several different options strategies, including:

- Short strangles

- Naked puts

- Naked calls

- Iron condors

- Ratio spreads

- Reverse Jade Lizards

Roman repeatedly emphasizes that the individual strategies themselves are not the point.

Each trade serves a purpose inside the portfolio. Some generate theta, others balance directional exposure, while others improve diversification or make better use of buying power.

When combined correctly, these trades create a portfolio with almost zero beta-weighted delta while generating approximately $100 of daily theta decay.

Managing the portfolio

Constructing the portfolio is only the first step.

As markets move, beta-weighted delta changes, so Roman continuously monitors and adjusts the portfolio.

Depending on market conditions, he may:

- Roll existing option positions

- Add new trades that offset directional exposure

- Use futures as temporary delta hedges

- Re-center positions after large market moves

His goal is not to predict where the market is going tomorrow. Instead, he wants to keep the portfolio balanced while continuing to harvest option premium through time decay.

Diversification comes first

Diversification is another core element of Roman's approach.

Rather than concentrating risk in one strategy or one market, he spreads positions across different:

- Underlying assets

- Option strategies

- Market sectors

- Expiration dates

He views every new position as another puzzle piece that should improve the portfolio as a whole.

This portfolio-first mindset is one of the biggest differences between his approach and the way many retail traders think about options.

Understanding the risks

Roman also makes it clear that a market-neutral options portfolio is not risk-free.

The biggest challenge comes during periods of rapidly rising volatility.

Because the portfolio is generally short option premium, sudden spikes in implied volatility can create significant temporary drawdowns. Black swan events therefore remain the greatest threat.

To manage those risks, he stresses the importance of conservative buying power usage, proper diversification, and, when appropriate, hedging positions to reduce portfolio exposure.

A portfolio-first mindset

Roman's biggest takeaway is that successful options trading starts with portfolio management – not trade selection.

Before looking for another strategy, he believes traders should first understand their beta-weighted delta, buying power usage, target theta income and overall market exposure.

Only then should they decide which strategies belong in the portfolio.

In Roman's view, iron condors, calendar spreads, strangles and countless other strategies are simply tools. The real edge comes from combining those tools into a well-balanced market-neutral options portfolio that consistently harvests option premium while minimizing unnecessary directional risk.

📚 Books recommended in this video

- Julia Spina: The Unlucky Investor’s Guide to Options Trading