Options trader Boomer Dan is known for creating strategies with memorable names, but behind the unusual title lies a thoughtful approach to managing risk. In this interview, he explains how the Burrito Butterfly works, why he developed it, and how he uses it in his own trading.

Learn about the Burrito Butterfly in this video

Boomer Dan

Boomer Dan (Dan Westbrook) has traded options since 2006 and specializes in theta-based trading strategies. Many traders know him from his educational content and his creative approaches to risk management using SPX options.

- Boomer Dan's website

- Watch our first interview with Dan: 0DTE levitation trades

The Burrito Butterfly

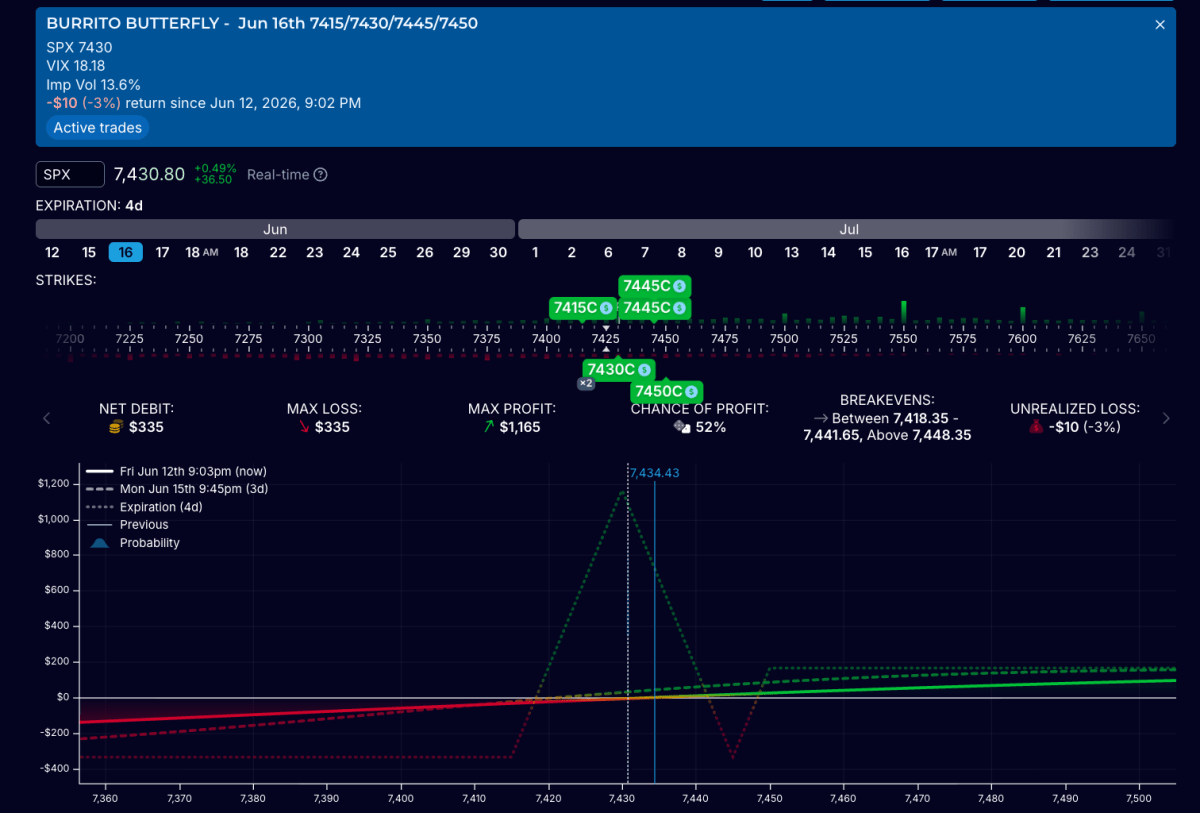

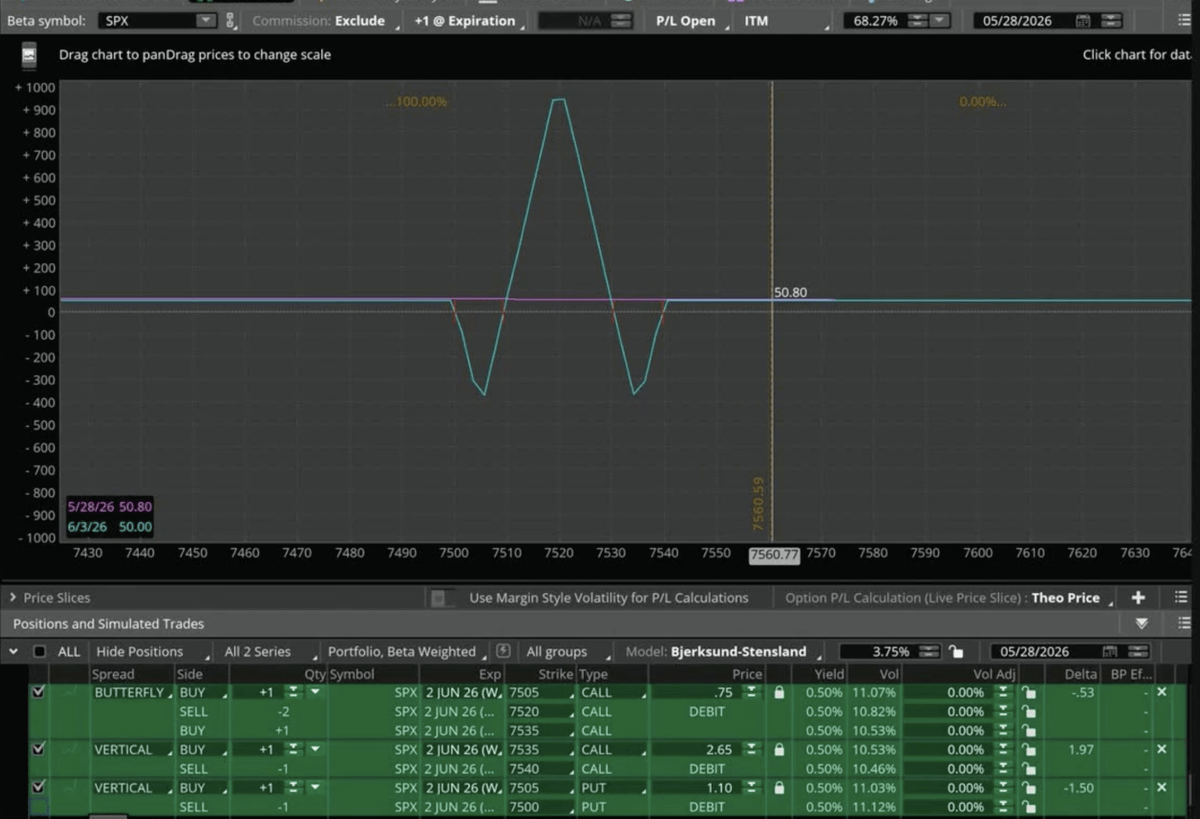

Dan starts with a 15-point-wide at-the-money SPX butterfly. He then adds a 5-point call debit spread on the upside if he is bullish and a put debit spread on the downside if he is bearish. The debit spread will have its long at the same strike as the long in the butterfly.

Most often he places the trade 2-3 days until expiraton.

The butterfly remains centered around the current market price while the debit spread provides upside or downside exposure if the index moves directionally.

The position benefits from two different forces:

- The debit spread gains value if he is right on the direction.

- The butterfly continues generating positive theta as time passes.

How the trade generates profits

The first phase of the trade is directional.

If price moves in the anticipated direction, the debit spread gains value while the butterfly continues to contribute positive theta. Dan typically looks for relatively modest returns, often targeting profits in the 5% to 10% range compared with the capital at risk.

At this stage, traders can simply close the position and take the profit. Dan's preferred approach, however, is to use the profit to turn the position into a “floating butterfly”, or a Burrito Butterfly.

Turning it into a Burrito Butterfly

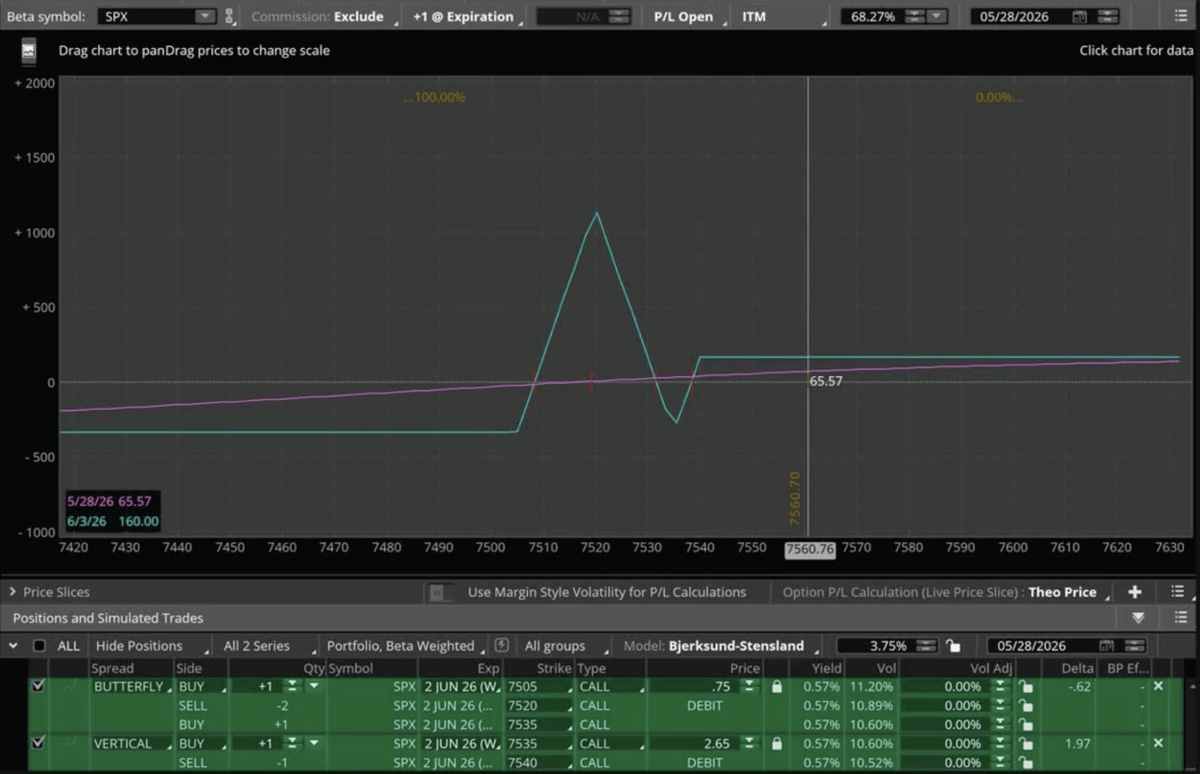

Once the initial directional trade has generated enough profit, Dan often adds a debit spread on the opposite side of the butterfly.

When this second debit spread is added at a favorable price, both sides of the position can potentially remain above the break-even line.

This creates what Dan refers to as a “floating butterfly.”

In this configuration, the trade can potentially remain profitable even if the market makes a large move in either direction. At the same time, the original butterfly spread remains in the center of the position and continues to benefit from theta decay.

Dan's goal is to create a position where downside risk has been significantly reduced while still maintaining additional profit potential if the market remains near the butterfly.

Once he has the “floating butterfly” in place, he is free to leave the position until expiration day.

Why the strategy moves slowly

A key premise of the Burrito Butterfly is that the position tends to move much more slowly than many directional options trades.

Throughout the interview, Dan repeatedly emphasizes that the current profit-and-loss line behaves very differently from the expiration graph. While the expiration graph may show what he calls the “Valleys of Death” between the butterfly and the debit spread wings, those losses typically do not appear immediately in the live position.

According to Dan's experience trading these structures, the current P&L line usually remains relatively flat or gradually rises as theta decay works in the trader's favor. The sharp losses shown on the expiration graph generally do not become a significant concern until the final hours of expiration day, when the current P&L line begins to converge with the expiration line.

This gives traders considerably more time to react than they would have with many other directional strategies. Rather than being forced into rapid decisions, the Burrito Butterfly is designed to provide opportunities to adjust, hedge, widen the profit tent, or lock in profits long before those valleys become a real threat.

For Dan, this slow-moving behavior is one of the strategy's biggest advantages and a major reason why he considers the Burrito Butterfly to be a relatively forgiving trade.

He underlines that it is important to pay attention on the expiration day. If the trade is at risk of falling into the “Valley of Death”, he will close it before the profit curve starts turning.

What if the market moves the wrong way?

One of the most interesting parts of the interview is Dan's discussion of trade management.

He openly admits that he does not believe he has a consistent edge in predicting market direction. Because of this, he focuses heavily on adjustments and risk control.

His first recommendation is simple: have a predefined stop-loss or “uncle point.”

Beyond that, he presents several adjustment techniques:

- Add the opposite debit spread to reduce further losses.

- Purchase a long option to flatten the risk curve.

- Add an additional butterfly spread to widen the profit tent.

Dan refers to adding additional butterflies as the “choo-choo train” adjustment because each new butterfly is like another car added to the train.

The objective is not necessarily to recover immediately but to create a position that is easier to manage and gives the trade more time to work.

The clawback adjustment

For traders who want to further fine-tune the position, Dan uses XSP options alongside SPX.

Because XSP is one-tenth the size of SPX, it allows him to make smaller adjustments. He uses additional debit spreads in XSP to raise the profit profile of the trade and reduce or eliminate losses that may have been locked into the position.

This process is known as the “clawback.”

According to Dan, the smaller size of XSP makes it useful for precision adjustments that would be difficult to achieve using only SPX contracts.

Risk profile

Dan considers the Burrito Butterfly to be a relatively conservative strategy once traders understand how it works.

On a risk scale from 1 to 10, he rates it around 3 to 4, although he suggests newer traders may view it closer to a 5 while they are learning the adjustment process.

The largest risk comes during the initial directional phase of the trade. If the market moves against the position and the trader fails to react, losses can build over time. Dan emphasizes that timely adjustments are a critical part of the strategy.

Key takeaways

The Burrito Butterfly is a creative variation of the traditional butterfly spread that seeks to combine directional trading with theta decay.

Rather than relying solely on market direction, the strategy focuses on gradually reducing risk as the trade develops. By adding debit spreads and adjusting the position over time, Dan attempts to transform a directional trade into a more neutral income-oriented position.

For traders who enjoy butterfly spreads and actively managing positions, the Burrito Butterfly offers an interesting framework for balancing risk, theta, and directional exposure.

[…] Boomer Dan: Burrito Butterflies […]