Every options trader eventually faces positions that move hard against them. In this interview, Zoheb Noormohamed walks through real trades in AMD, Walmart, and Microsoft to show how he adjusts losing positions, collects credits, and reduces directional risk when trades move against him.

Get tips about how to adjust losing options trades in this video

Zoheb Noormohamed is a London-based options trader and YouTube educator who focuses heavily on short premium strategies such as strangles, short puts, and straddles. He uses a mechanical adjustment process to manage losing options trades and reduce directional exposure.

- Zoheb on YouTube

- Zoheb Noormohamed: How I trade the 1-1-1 strategy

Why adjusting losing options trades matters

One of the biggest themes throughout the interview is that successful options trading is not only about finding good entries.

According to Zoheb, traders should already know how they plan to adjust losing options trades before they enter a position. Many traders focus heavily on setups and strategies, but very few think carefully about what they will do if the stock suddenly makes a large move.

Zoheb mainly trades undefined risk positions such as short puts and strangles. These trades benefit from time decay and elevated implied volatility, but they also require active management when positions move deep into the money.

Rather than reacting emotionally, Zoheb follows a repeatable process designed to:

- Reduce delta exposure

- Collect additional credits

- Widen break-even points

- Improve the probability of recovering the trade

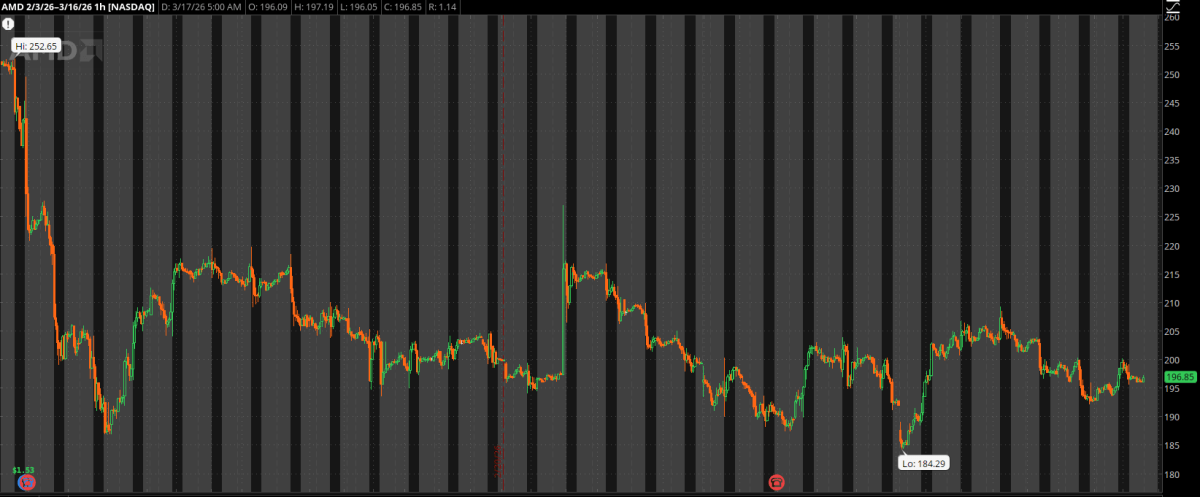

The AMD trade: How he repaired a losing options trade

The first example in the interview is an AMD short put entered before earnings.

Zoheb sold a short-duration put just before the earnings announcement in order to take advantage of high implied volatility. Initially, the trade looked attractive because AMD would have needed to make a very large move lower before the short put became threatened.

Instead, AMD dropped sharply after earnings and quickly moved deep into the money.

At that point, Zoheb had two choices: close the position for a large loss or begin adjusting the trade.

He chose to roll the short put down to a lower strike and further out in time while collecting additional premium. As AMD continued falling, he added the call side and converted the position into a strangle.

This adjustment process had two major goals:

- Collect more premium

- Reduce directional delta exposure

Throughout the trade, he repeatedly rolled down the untested side while continuing to collect credits.

Eventually, despite the original trade moving heavily against him, Zoheb was able to close the position for an overall profit.

You get all the details of his adjustments in the video.

Using strangles to defend losing positions

A major part of Zoheb’s strategy involves using strangles.

A strangle consists of selling an out-of-the-money call and an out-of-the-money put at the same expiration. The position is typically opened as a delta-neutral trade.

When one side becomes challenged, Zoheb often rolls the untested side closer to the current stock price.

If the stock moves down and threatens the put side, he rolls down the call side. If the stock rallies and threatens the call side, he rolls up the put side.

The purpose is to:

- Collect additional credits

- Flatten out delta exposure

- Widen break-even points

- Increase the probability of recovery

Throughout the interview, Zoheb repeatedly emphasizes that the process should remain mechanical rather than emotional.

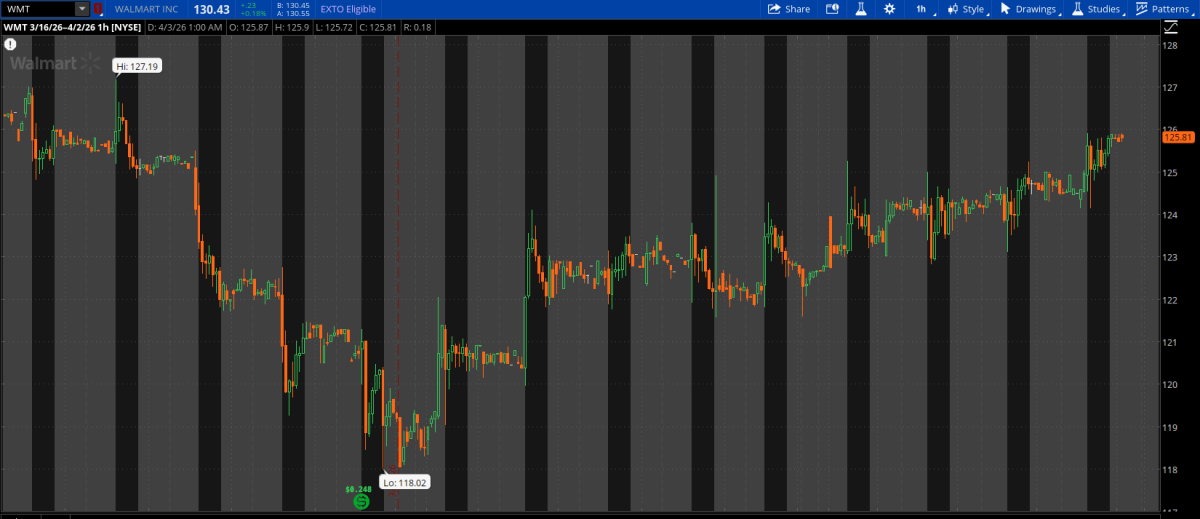

The Walmart trade: From strangle to inversion

The second major example involves a Walmart short strangle.

Zoheb initially opened a standard short strangle around the 20 delta level. But Walmart began moving lower and challenged the put side of the position.

As the stock continued moving down, Zoheb repeatedly rolled down the call side to collect more credits and reduce directional exposure.

Eventually, the trade evolved from:

- A standard strangle

- To a straddle

- To an inverted strangle

An inverted strangle occurs when the put strike becomes higher than the call strike.

Although many traders would find this uncomfortable, Zoheb explains that strike locations become less important once enough premium has been collected.

Instead, he focuses mainly on where the break-even points are located.

Even though the trade eventually became inverted, the accumulated credits allowed him to close the trade for a profit.

You get all the details of his adjustments in the video.

The Microsoft trade: Managing a live losing position

The final example in the interview is a Microsoft strangle that was still open at the time of recording.

The trade started as a standard 45-to-60-day short strangle with roughly 20 delta exposure on both sides. But as Microsoft rallied sharply higher, the call side moved deep into the money, and the position became increasingly directional.

Rather than closing the trade, Zoheb focused on reducing delta exposure mechanically. He repeatedly rolled up the untested put side, collected additional credits, and improved the break-even points.

A key factor was the upcoming Microsoft earnings event. Because implied volatility was elevated ahead of earnings, Zoheb decided to wait before rolling the position further out in time in order to collect more premium.

Later in the interview, after earnings, the trade had improved significantly. Although the position had previously shown a large unrealized loss, the adjustments and additional credits helped bring the trade back into profitability.

You get all the details of his adjustments of this trade in the video.

Delta management is the key

Zoheb explains that good delta management is crucial when adjusting losing options trades.

When a short premium position becomes too directional, traders become exposed to increasingly painful price swings. Zoheb, therefore, focuses heavily on flattening delta exposure whenever possible.

He explains several methods he uses:

- Rolling positions further out in time

- Opening the opposite side of the trade

- Rolling the untested side closer to the current price

- Collecting additional credits during adjustments

The goal is not always to immediately return the trade to profitability. Instead, the objective is often to improve the structure enough for the position to recover later.

Defined risk versus undefined risk trading

Zoheb also discusses the differences between defined risk and undefined risk strategies.

He explains that spreads and iron condors can be more difficult to adjust because the long options reduce flexibility during adjustments.

Still, many of the same principles can apply.

For example, traders with a losing put credit spread may sometimes add a call spread and convert the trade into an iron condor while collecting additional premium.

Although defined-risk traders may not always fully recover losing positions, adjustments can still help reduce the maximum loss.

Staying mechanical under pressure

One of the strongest lessons from the interview is the importance of staying mechanical when trades move against you.

Large losing positions can create emotional pressure and tempt traders to panic or abandon their plan.

Zoheb instead focuses on repeating the same process:

- Reduce delta exposure

- Collect credits

- Widen break-even points

- Stay patient

As he says in the interview: “Losing trades can be repaired.”

[…] Zoheb Noormohamed: How to adjust losing options trades […]