Most traders approach earnings by trying to forecast where a stock will move. AJ Brown takes a different path. His earnings options strategy is built around profiting from predictable changes in option prices before and after earnings announcements.

Learn about the earnings options strategy in this video

A.J. Brown

AJ Brown is the founder of The Trading Trainer and has been teaching options trading for more than two decades. He specializes in identifying repeatable patterns in the options market and building strategies around them rather than predicting market direction. In addition to running his educational business, he also leads a nonprofit program that teaches options trading to underserved youth in Chicago.

- A.J. Brown on YouTube

- The Trading Trainer

- Our first interview with A.J. Brown: A VIX hedge for options sellers

Why this earnings options strategy works

In this interview, A.J. explains how he uses calendar spreads during earnings season to take advantage of implied volatility crush while carefully managing risk.

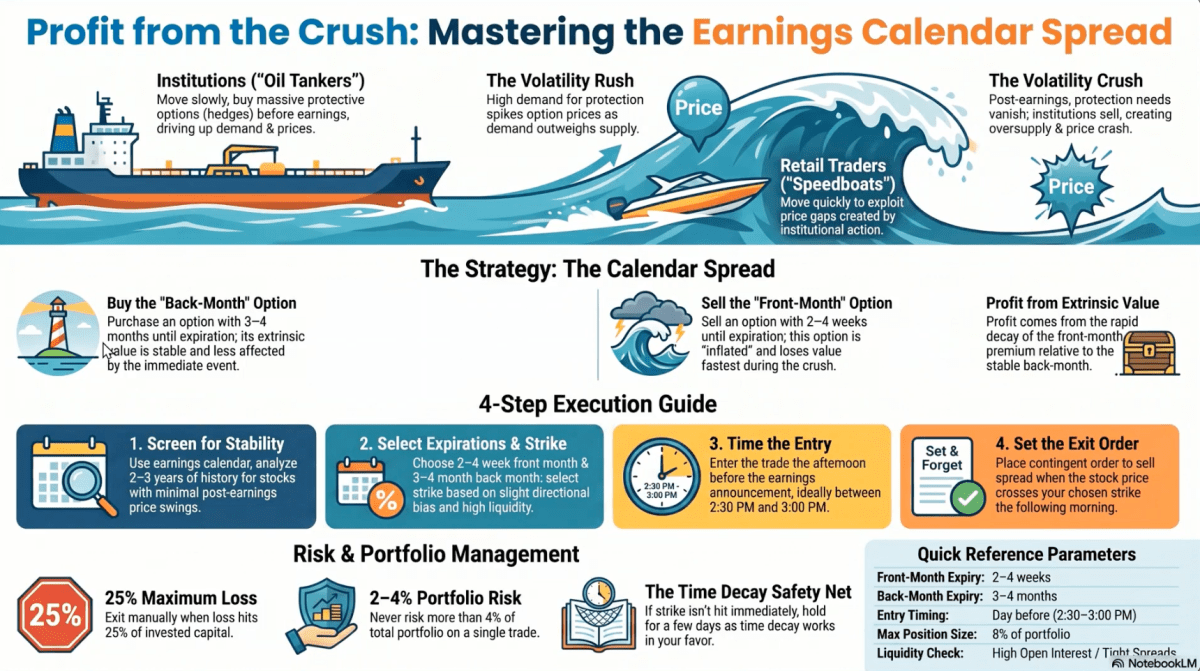

The foundation of A.J.'s approach is the behavior of institutional investors around scheduled events.

Before earnings announcements, many large investors buy short-term options to protect existing stock positions. This increased demand pushes up implied volatility, making those options more expensive.

After the earnings announcement, uncertainty disappears. If the stock does not make a dramatic move, those protective options quickly lose value as implied volatility falls.

Rather than trying to predict whether the stock will rise or fall, AJ's earnings options strategy focuses on capturing this decline in option prices.

Using calendar spreads to profit from volatility crush

To trade this pattern, A.J. uses calendar spreads.

A calendar spread consists of buying and selling options with the same strike price but different expiration dates.

His typical setup is to buy an option three to four months from expiration while simultaneously selling a shorter-term option that expires in roughly one to four weeks.

The longer-dated option tends to remain relatively stable because it is less affected by the earnings event. The shorter-dated option, however, often experiences a significant drop in value after earnings as implied volatility contracts.

Because both options use the same strike price, much of the intrinsic value offsets itself. The trade therefore becomes primarily an opportunity to profit from changes in extrinsic value, time decay and implied volatility.

OptionStrat

is the option trader's crucial toolkit. Trade smarter with the best visualization and analysis tools available.

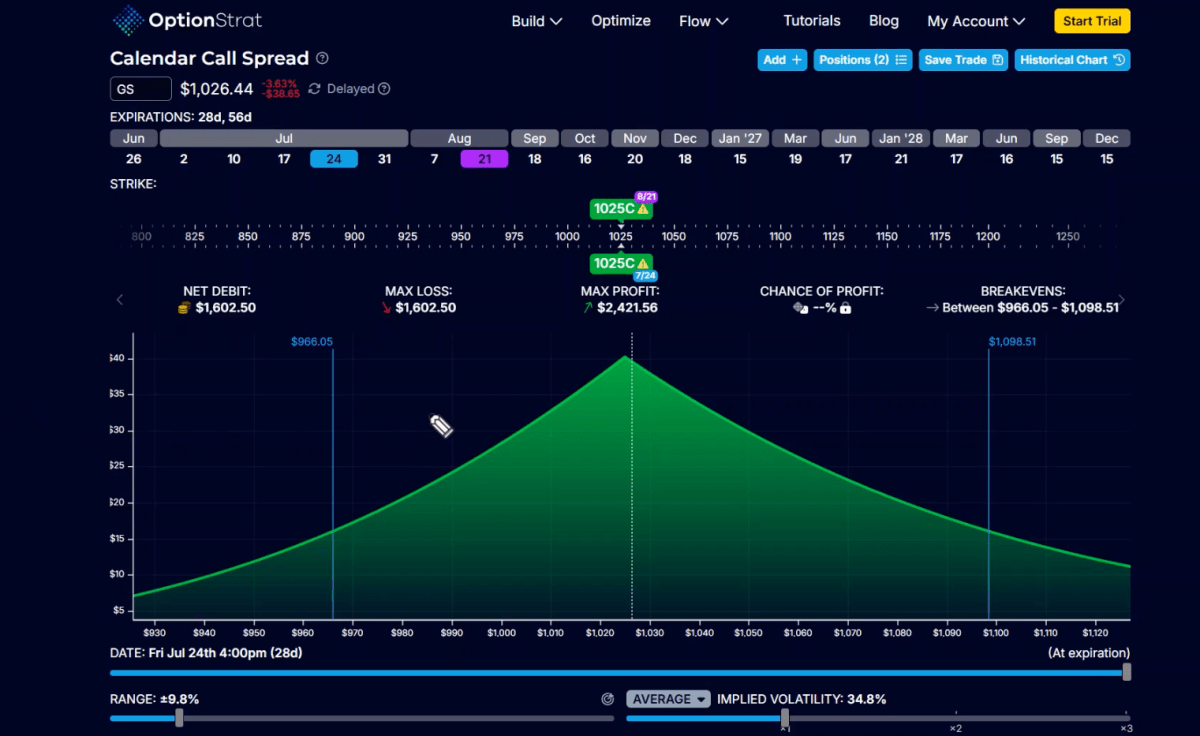

An example trade on Goldman Sachs

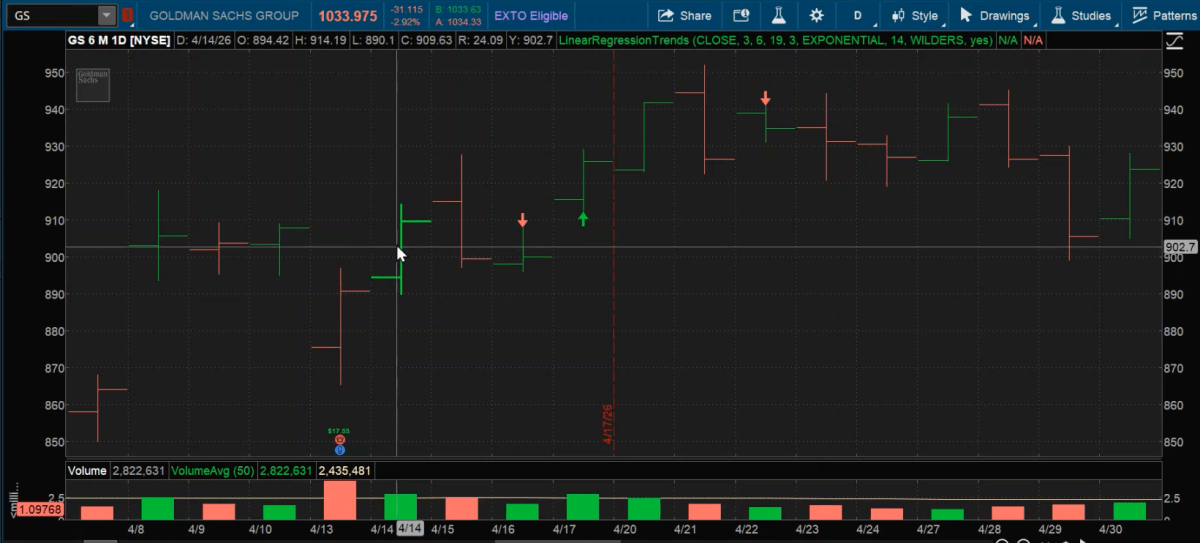

To illustrate the strategy, A.J. walks through a trade he made on Goldman Sachs (ticker GS) during the April earnings season.

The earnings were announced before the market opened on Monday, April 13, 2026. A.J. always places his trades during the last session before the earnings announcement, which was Friday, April 10.

- He chose to open a calendar at-the-money with strike 905

- The short call had expired on April 24 and was sold for $27.14. The long call expired on June 18 and was bought for $51.85. The total debit for the calendar was $24.71.

- A.J. main rule is to close the trade when the price of the stock touches the strike price.

- This happened on Tuesday, April 14, the day after the earnings announcement. A.J. then could buy back the short for $21.55 and sell the long for $47.72. The total credit was $27.14.

- A.J. thus made $2.43, or 9.8% of his max risk, in just four days.

A.J. uses this trade to demonstrate how relatively modest but repeatable gains can accumulate over many earnings opportunities.

Finding the right earnings trades

According to A.J., stock selection is one of the most important parts of the strategy.

He looks for companies that have historically shown relatively modest price reactions after earnings. His goal is to find stocks that may fluctuate briefly but generally return to their previous trading range within a few days.

Before entering a position, he reviews approximately the previous eight earnings cycles and also considers current news affecting both the company and its sector.

If he expects unusually large price movements because of major news or uncertainty, he simply avoids the trade. In those situations, he believes strategies such as straddles or strangles are more appropriate.

- Other earnings trades interviews on Theta Profits:

- Amin Khribi: Four costly earnings trades mistakes every options trader should avoid

- Brian Terry: Post-earnings credit spreads

- Daniel Nikolaides: A complete guide to trading the IV crush

- Theta LIVE: Trade earnings with a plan

EarningsWatcher

…turns messy earnings volatility into clear, research-backed setups – so you can trade with consistency, not luck. You get numerous earnings data for each underlying – and a repeatable workflow for earnings trades, from idea to execution to improvement.

Entry and exit rules

AJ usually enters his calendar spreads during the final trading session before the earnings announcement, often during the last couple of hours before the market closes.

He generally chooses an at-the-money strike price, although he may adjust it slightly if he has developed a directional bias after following a particular stock for a long time.

Once the trade is open, he immediately places a good-until-cancelled exit order.

His preferred exit occurs when the underlying stock later crosses the strike price of the calendar spread. For many trades, this happens within only a few trading days.

Rather than chasing maximum profits, he aims for consistent gains, typically around 5% to 10% on the spread, while repeating the process across multiple earnings opportunities.

Managing risk when the earnings options strategy goes wrong

A.J. emphasizes that not every earnings trade works as planned.

If the stock moves too far away from the strike price or the front-month option approaches expiration before the planned exit, he may close only the short option while continuing to hold the longer-dated option.

This effectively transforms the position into a directional trade and gives additional time for the market to recover.

He also stresses proper position sizing throughout the interview. Instead of deciding how many contracts to trade based on confidence, he calculates position size according to the maximum amount he is willing to lose as a percentage of his overall portfolio.

For A.J., disciplined risk management is more important than finding the perfect setup.

The key lessons

AJ Brown's earnings options strategy is designed to capitalize on one of the most consistent patterns in options markets: implied volatility often rises before scheduled events and contracts immediately afterward.

By combining careful stock selection with calendar spreads, disciplined entries and exits, and sound risk management, he seeks to profit from option pricing rather than trying to predict the market's next move.

For traders looking for an earnings options strategy that relies more on volatility than direction, calendar spreads provide an interesting alternative to traditional earnings trading approaches.

📚 Book recommended in this video

- Sheldon Natenberg: Option Volatility & Pricing