This interview with Brendan Johns breaks down his high-probability Trojan Horse 0DTE Iron Condor strategy and how gamma levels can improve both entries and exits.

Learn about the Trojan Horse 0DTE Iron Condor

Brendan Johns

Brendan Johns is an experienced retail options trader based in Philadelphia who specializes in short-term options strategies. Over the past year, he has refined a 0DTE iron condor approach focused on volatility and intraday price behavior.

What is a 0DTE Iron Condor?

A 0DTE Iron Condor is an options strategy where you sell both a call spread and a put spread that expire on the same day. The goal is to profit from price staying within a defined range while time decay (theta) works in your favor.

In this case, Brendan trades primarily on SPX and opens positions shortly after market open. The strategy is built to take advantage of intraday volatility and rapid time decay.

At a basic level, the structure includes:

- Selling out-of-the-money call and put spreads

- Defining risk with long options further out

- Letting theta decay drive profits throughout the day

Even without active management, Brendan shows that this type of 0DTE iron condor can be profitable over time.

The core idea behind the strategy

The foundation of this Trojan Horse 0DTE Iron Condor strategy is simple: define a range where the price is likely to stay during the trading day and collect premium from both sides.

Brendan’s baseline setup includes:

- Selling the 8-delta options on both sides

- Buying the 7-delta options to define risk

- Entering trades around 9:31 AM

- Only trading when VIX is between 19 and 40

This creates a high-probability range where the market is expected to stay within the defined boundaries.

The simplicity of this setup is important. Brendan emphasizes that even a mechanical version of this strategy – without active management- has historically been profitable.

How gamma levels improve the edge

What turns this into a “Trojan Horse” strategy is the use of gamma exposure (GEX) and heat maps.

Gamma levels represent areas where market makers are forced to buy or sell as the price moves. These zones can act as intraday support and resistance.

Brendan uses this information to:

- Adjust where he places his strikes

- Capture areas of expected price deceleration

- Avoid zones where the price may accelerate

In simple terms:

- Positive gamma → price tends to slow down or reverse

- Negative gamma → price tends to accelerate

By positioning the Iron Condor around these levels, the strategy increases the probability that the price stays within range.

Entry timing and conditions

Timing is critical in the Trojan Horse 0DTE Iron Condor strategy.

Brendan typically enters trades:

- Right after market open

- When volatility is elevated (VIX above 19)

- Avoiding extreme volatility spikes

He also filters out days with major macro events such as Fed announcements or significant geopolitical news.

The goal is to trade in environments where volatility premium is high—but not chaotic.

Trade management and exits

Unlike passive strategies, this 0DTE Iron Condor requires active management.

Key principles include:

- Targeting 80–85% of maximum profit

- Monitoring gamma levels throughout the day

- Exiting early if price breaks key zones

Instead of fixed stop-losses, Brendan uses market structure and gamma behavior to decide when to exit.

If price moves aggressively beyond expected levels—especially early in the day—the trade is typically closed to limit losses.

- Watch other interviews about 0DTE trading

- Jamaal Ghurani: 0DTE Butterfly

- Eddy Li: Scalping SPX options

- John Einar Sandvand: 0DTE Breakeven Iron Condor

Hedging with debit spreads and butterflies

When the market moves against the position, Brendan may hedge rather than immediately exit.

Two common adjustments are:

- Debit spreads to hedge directional risk

- Butterflies to “pin” price around key levels later in the day

Debit spreads are typically used earlier in the session when moves start to accelerate. Butterflies are more effective later in the day when time decay increases rapidly.

These adjustments help reduce drawdowns and improve overall consistency.

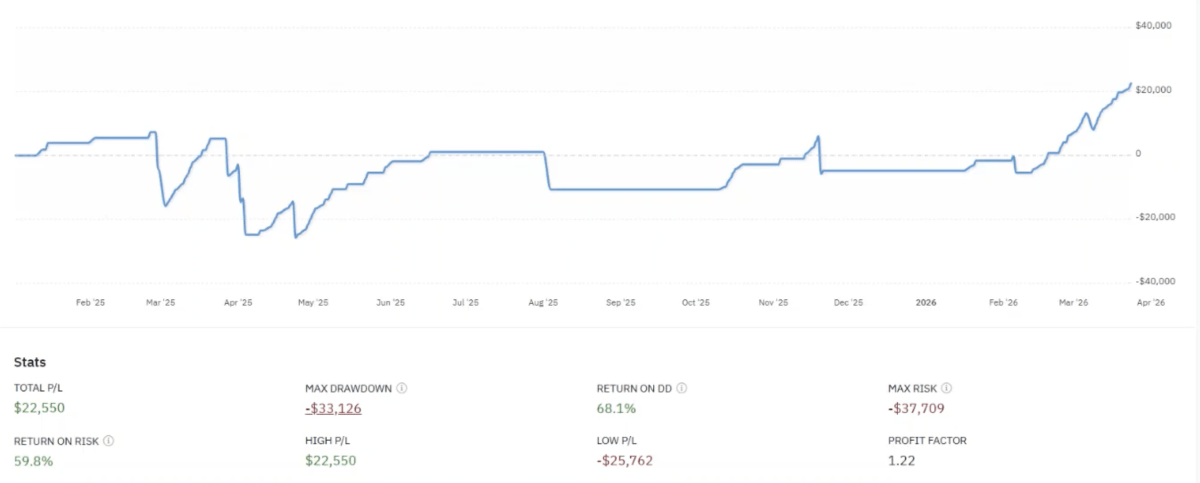

Results from the strategy

Brendan has been trading this 0DTE Iron Condor strategy for about a year, with a strong focus on refining it during the most recent quarter. In Q1 alone, the strategy delivered a 40% return on his trading account.

On a per-trade basis, the setup typically collects around $100–$150 in premium per contract, while the theoretical maximum loss can be several times larger. However, through active management and hedging, his realized losses have been significantly lower than the theoretical maximum.

The strategy also benefits from a high win rate – often above 90% – but this comes with the trade-off of occasional larger losses. This balance between frequent small wins and controlled losses is a key part of the overall performance.

Risk and key takeaways

This is not a low-risk strategy.

Brendan rates it as an 8 out of 10 in risk due to:

- Large potential losses relative to gains

- The need for constant monitoring

- Sensitivity to sudden market moves

There are two main lessons from this approach.

First, backtesting is essential. Even simple strategies should be validated with data before risking capital.

Second, understanding market maker positioning through gamma levels can significantly improve trading decisions.

The combination of a structured 0DTE iron condor and informed trade management creates a powerful framework—but it requires discipline, attention, and risk awareness.

For traders looking to refine their 0DTE approach, this strategy offers both a solid foundation and a clear path to optimization.

📚 Book recommended in this video

- Colin Bennett: Trading Volatility