Volatility spikes are the moments when many options strategies feel hardest to stick with. In this interview, AJ Brown explains how he approaches the VIX not as something to predict, but as something to structure around, using a hedge designed to quietly do its job until markets become chaotic.

Watch A.J. Brown describe his VIX hedge

A.J. Brown

A.J. Brown is a long-time options trader and educator who has been trading since the late 1990s. He is known for a disciplined, rule-based approach to trading, with a strong emphasis on structure, repeatability, and portfolio-level risk management. In addition to trading his own account, AJ runs Trading Trainer, where he focuses on helping traders build strategies that can survive multiple market cycles.

Why options sellers need a VIX hedge

Selling options for income works well when markets are stable. Time decay is predictable, volatility is contained, and strategies such as credit spreads and iron condors behave as expected. The problem is that volatility does not stay contained forever.

When markets sell off sharply, implied volatility expands quickly. Losses in short premium positions often appear simultaneously across multiple trades, and many options sellers discover that they are effectively short volatility without realizing it. This is where a VIX hedge for options sellers becomes valuable.

A.J.’s core argument is simple: volatility spikes are inevitable. A hedge is not about predicting when they will happen, but about being prepared when they do.

- Watch other video interviews from Theta Profits:

- The Options Seller: Options on futures

- Levi Woods: The ratio diagonal

- Doc Severson: 0DTE Iron Fly

- Carl Allen: Rolling Put Credit Spread

How the VIX behaves during market stress

A key foundation of the strategy is understanding how the VIX behaves over time. The VIX reflects implied volatility in S&P 500 options and is often described as a measure of fear versus confidence.

Historically, the VIX is mean-reverting. It spends most of its time in a relatively narrow range and rarely stays extremely low or extremely high for long. However, its movements are not symmetrical. Confidence builds slowly, but fear arrives fast. When uncertainty hits the market, the VIX can spike sharply in a matter of days.

This behavior makes the VIX difficult to trade directionally, but well-suited for structured hedging strategies that are designed to benefit from sudden volatility expansion.

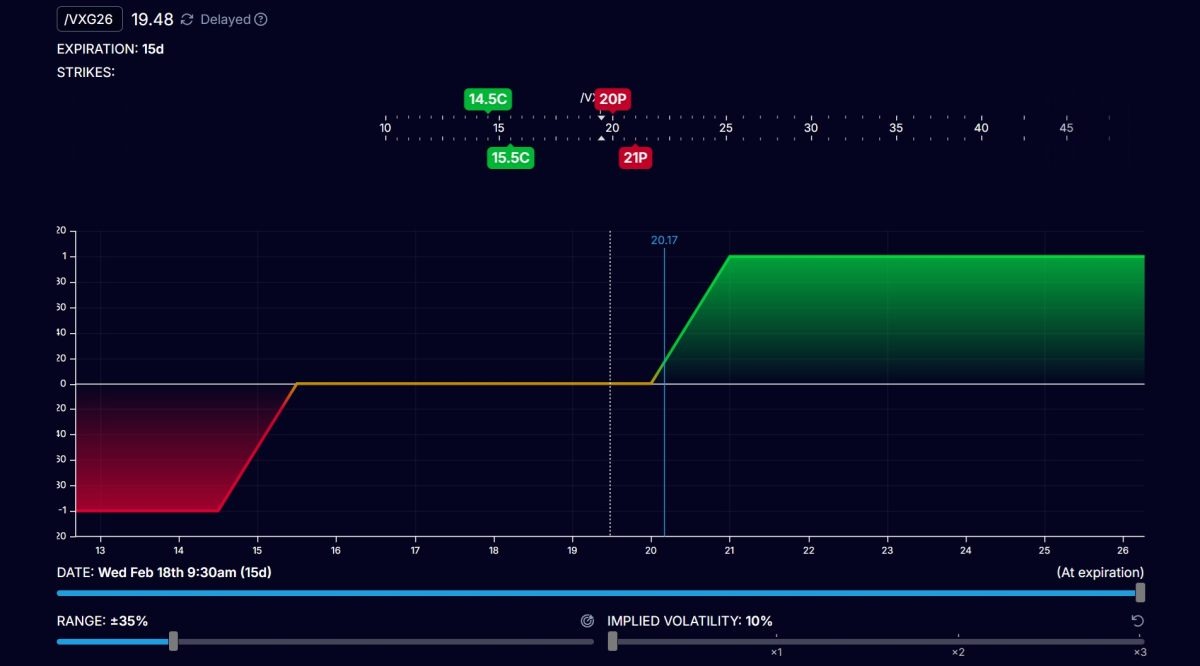

The dual-vertical VIX hedge: structure and setup

AJ’s hedge uses a simple but very deliberate structure built with VIX options. It combines two vertical spreads with the same expiration.

The first leg is a debit call spread placed below current VIX levels. In the example trade used in the video, be buys a 14.50 call and sells a 15.50 call. This spread benefits directly from a rise in the VIX and is part of the trade that produces large gains during volatility spikes.

The second leg is a put credit spread placed above current VIX levels. In the example from the video, this could mean selling the 20.50 put and buying the 19.50 put. This spread generates premium and is used to help finance the cost of the call spread.

The goal is to structure the two spreads so that the credit received from the put spread roughly offsets the debit paid for the call spread. When done correctly, the net cost of the entire position is close to zero, or even slightly positive.

Days to expiration and strike selection

AJ typically uses expirations in the range of two to five weeks. This window provides enough time for volatility to expand, while avoiding excessive theta decay or the need to hold the hedge for long periods.

Strike selection is deliberate. The call spread is placed below current VIX levels, where it will benefit quickly from a volatility spike. The put spread is placed well above the current VIX, in an area where the VIX rarely spends much time.

This creates a wide “middle zone” where the trade does very little. If the VIX remains between the two spreads, the position is expected to break even or produce a very small gain.

Entry mechanics and timing

AJ does not place this hedge randomly. He looks for periods of volatility compression, when the VIX is near the lower end of its recent range.

To help with timing, he uses a fast MACD signal on the VIX to identify potential volatility bottoms. The idea is to enter when volatility is low, and signs suggest it may be ready to expand. In practice, he often enters the call spread first and then adds the put credit spread after a small move higher in the VIX to improve pricing.

This approach avoids chasing volatility after fear has already arrived. How he uses the MACD signal is described more in detail in the video.

Exit mechanics and trade management

Most of the time, nothing dramatic happens. If the VIX remains in the middle range through expiration, both spreads expire with little or no value, and the trade ends near break-even. This is the expected outcome in calm markets.

When the VIX spikes sharply, the call spread can move quickly toward its maximum value. In those cases, AJ does not wait for expiration. He typically closes the entire position early, locking in gains that can be several times the initial cost of the trade.

There is no need for constant adjustments or active management. The hedge is designed to be simple, defined-risk, and easy to repeat.

Why breaking even is the objective

One of the most important lessons from the interview is that a hedge should not be judged by how often it makes money. Its purpose is to protect the portfolio when other strategies struggle.

By accepting frequent break-even outcomes, this VIX hedge avoids becoming a drag on performance. At the same time, it retains the ability to deliver meaningful gains during periods of market stress, when those gains matter most.

Who this VIX hedge is best suited for

This approach is best suited for options sellers who rely on short premium strategies for income and want a structured way to manage volatility risk. It is particularly useful for traders who find that market crashes lead to emotional decision-making or abandoning otherwise sound strategies.

Rather than acting as a standalone profit engine, the hedge functions as portfolio insurance. It helps smooth returns across market cycles and allows traders to stay disciplined when markets become unpredictable.

Is there any reason you are using itm spreads vs. the otm synthetic equals? (otm put credit spread below and otm call debit spread above). Seems like you would avoid slippage of having to close trades that are expiring worthless. I don’t trade VIX so just curious what I am missing.

[…] Our first interview with A.J. Brown: A VIX hedge for options sellers […]