Originally published: 2024 Updated: February 2026 after more than 9,000 trades

For almost five years, I have traded the 0DTE Breakeven Iron Condor on SPX. Over more than 9,000 trades, it remains my most profitable options trading strategy, and it has been consistently profitable throughout that period.

In this video and article, I break down exactly how the strategy works, how I manage risk, what the real risks are, and what I have learned after thousands of live trades.

0DTE Breakeven Iron Condor: How I trade it

These are my key statistics

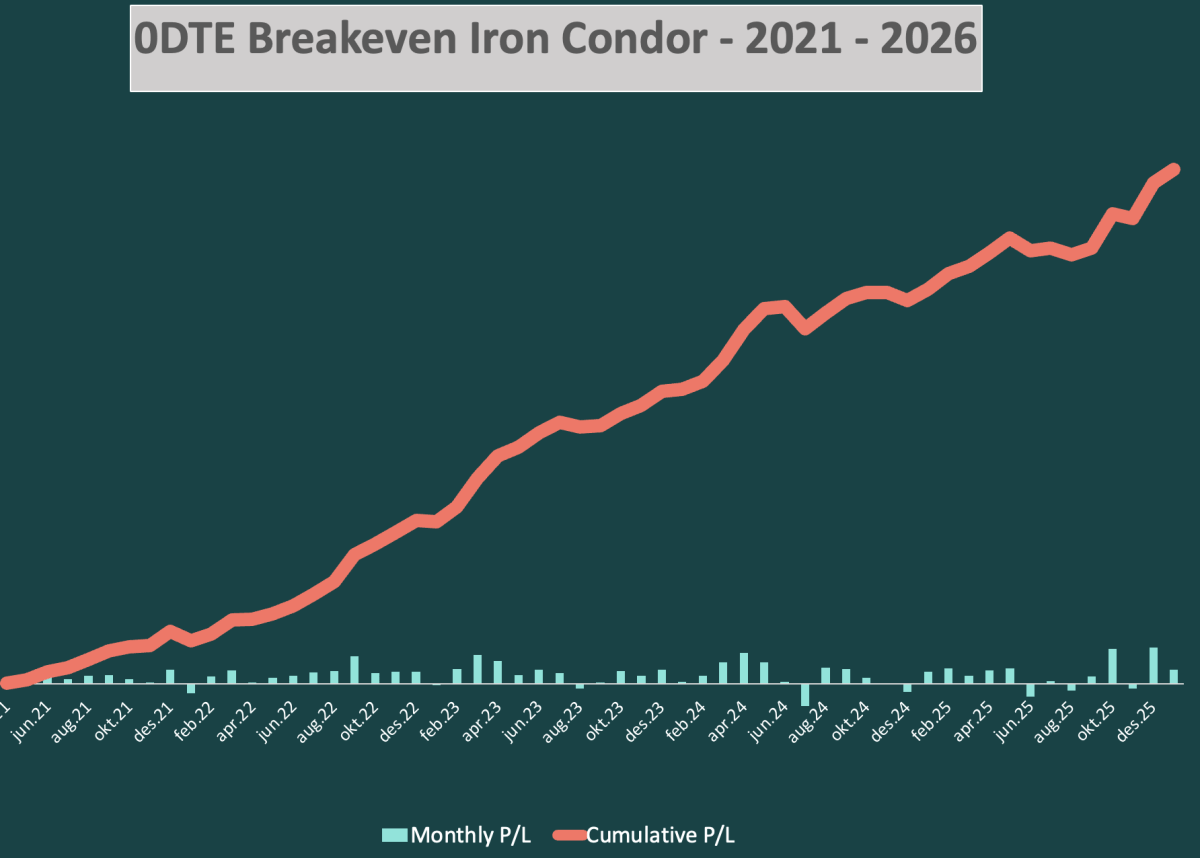

– I have done a total of 9,100 trades with this strategy from April 2021 until February 2026.

– 40% of the trades are wins and 60% are losses. However, the strategy remains profitable because the average win is more than double the average loss.

– 49 of 57 months have been profitable

– The average Premium Capture Rate (PCR) is 5.65%. The average P/L per trade is 0.28%.

The graph illustrates how the 0DTE Breakeven Iron Condor strategy has performed since I started trading it in April 2021.

The 0DTE Breakeven Iron Condor strategy

Let's go straight to the point about what the 0DTE Breakeven Iron Condor strategy is:

– It consists of selling Iron Condors on SPX with deltas typically between 10 and 15 – with expiration the same day – collecting the same premium on both sides

– The trades have very tight stop-losses – set separately for each side equal to the total premium collected for the Iron Condor. This limits the potential loss on each trade.

– The stop-losses can be tightened throughout the day to manage the total risk and secure profits.

The tight stop-losses mean that the loss will be close to zero if the stop-loss hits on one side, hence the name “Breakeven Iron Condor”. In principle, you will only lose on the strategy if the stop losses hit on both sides of the Iron Condor. This has happened in 8.6% of my trades. This number is higher than in the first years of trading the strategy – an indication of more intraday volatility.

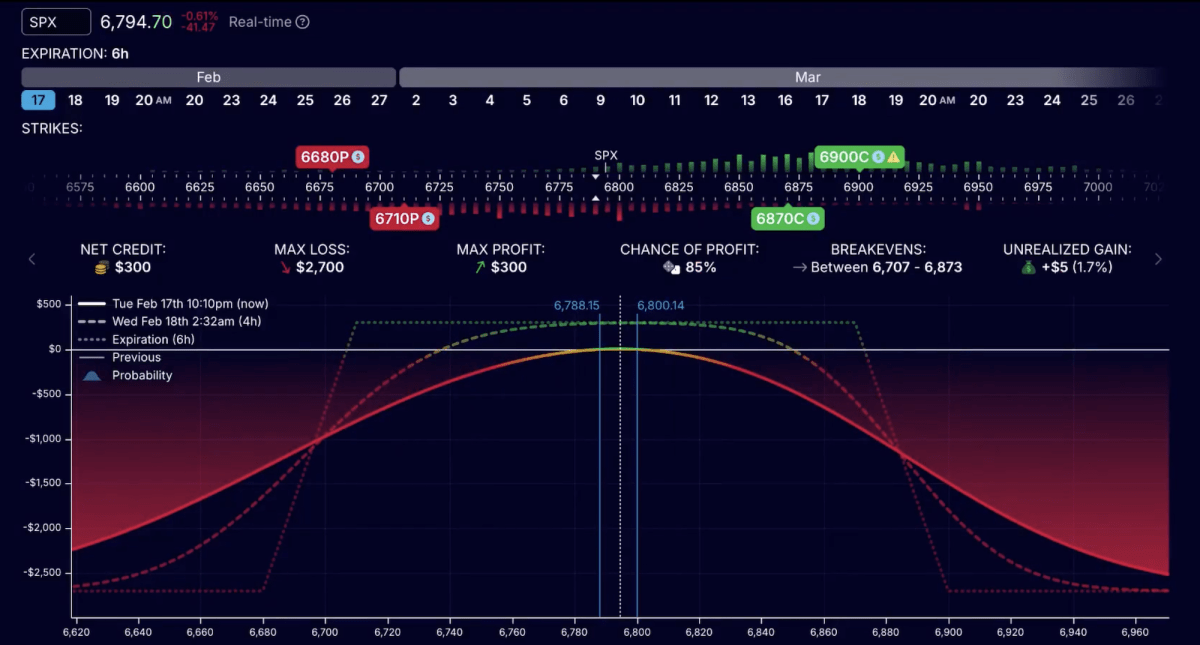

Example of a 0DTE Iron Condor – used in the video and visualized through OptionStrat. The trade was opened about 35 minutes after the market open on February 17, 2026. when SPX was at approximately 6,800. We have sold a put credit spread 6710/6680 and a call credit spread 6870/6900 and collected $150 on each side – a total of $300. The same trade at expiration if the market has stayed at the same level. Illustration: OptionStrat.

Here are some of my rules for entering and exiting the trades:

– I enter trades at regular intervals throughout the day – but with at least 30 minutes between. My normal set-up is to enter about once per hour. I try to get equal credit on both sides of the Iron Condor.

– The shorts will usually be between 10 and 15 delta – and the distance to the longs normally 30 points. But I will adjust this to get equal credit on both sides. In most cases I will collect between $100 and $200 on each side of the Iron Condor, in other words $200-$400 in total.

– I immediately set stop-losses on both sides separately. I have chosen to only set the stops on the shorts. The longs will then be closed manually shortly after a stop-loss hit. I have found that this reduces slippage and bad fills. i set my stop-losses as a combination of a stop limit order and a stop market order, using the OCO (One Cancels the Other) functionality. (see demo below)

– If set on the spreads, the stop-losses on each side should equal the total premium I received on the Iron Condor. When set on the shorts only, I adjust for the value of the longs. Here is an example: Let's say I collect 300 dollars for the full Iron Condor, or 150 dollars on each side. On the put side the short was sold for 220 dollars and the long bought for 70 dollars. I will then set the stop-loss on the short put at around 400 dollars – essentially equal to the total premium plus the value of the long put plus an estimate of how much the long will increase in value if the market moves close to the stop level. In this example I have estimated this “extra value” to 30 dollar. So my calculation is: $300 + $70 + $30 = $400.

– I also set a take-profit level of 5 cents for each short. I could let them expire worthless, but I like this way of reducing the total risk as the day passes. Very often I will reuse the longs for new trades.

– The stop-losses might be tightened throughout the day for two reasons. The first is to compensate for the decay of the longs due to theta. To use the previous example: After a couple of hours, the long may only be worth 40 dollars. Then I will tighten the stop-loss on the short put to 360 dollars. The other reason for tightening the stop-losses is to secure some profit and also out of consideration for the total risk of all my open positions.

Demo: Watch how I set my stop loss orders in Thinkorswim

How I manage the risk with the 0DTE Breakeven Iron Condor strategy

Here are some of my main rules for risk management:

– I never risk more than a maximum of 1-2% of my account on any single day. This is the main principle for how many trades I put on and how I manage the positions. I will rarely use more than 50% of my total buying power. The risk is measured as a percentage of what I would lose if all stop losses were hit.

– Regularly throughout the day, I ask myself: What is the WORST that can happen with my current positions? The answer to this question guides to what extent I will put on new trades and how I manage my existing positions.

– I keep adjusting my stop losses to control my maximum losses and ensure profits.

– I do many, but small trades. However, I let there be at least 30 minutes – usually 1 hour – between each trade. This allows me to enter the positions at different market levels. The number of trades will vary – depending on how I see the market and my total risk.

The biggest risk of the strategy is double stop losses, when the stops on both the put and the call side hit. This is when a trade sees a real loss. In my trading this has happend in about 8.6% of my 9,100 trades. This number has grown over the years, a possible sign that intraday volatility is increasing.

My results trading 0DTE Breakeven Iron Condor

I use two different metrics to measure my results of daytrading strategies. Both are solid ways of analyzing the results over time, in my experience.

1. Net profit per average trade

This metrics measures my net profit (after commissions and fees) as a percentage of the risk taken (spread width minus premium).

Over all my 9,100 trades, this has averaged around 0.28% per trade.

It sounds small.

But remember:

This is intraday capital deployed repeatedly. Multiply it with roughly 250 trading days in a year, and the results are more impressive.

The average monthly net profit per trade from May 2021 to January 2026.

2. Premium capture rate

This metric shows the net profit divided by total premium collected.

This measures how efficiently premium is retained over time.

Both metrics tell the same story:

The edge is small — but consistent.

And consistency compounds.

The average Premium Capture Rate for all my 9,100 trades have been 5.65%.

The average monthly Premium Capture Rate from May 2021 to January 2026.

The profitability of 0DTE Breakeven Iron Condor

Let's sum up with a few words about the profitability of this strategy.

As pointed out, around 6 of 10 trades are losses. But the average win is more than twice as big as the average loss.

And with those statistics, you can measure the expectancy of the strategy by using the standard formula:

Expectancy = (win rate X average size of the win) – (loss rate X average size of the loss)

Having logged 9,100 trades, I feel confident that the strategy has a solid long-term profitability.

One well-known version is the MEIC strategy – or Multiple Entries Iron Condors. Texas retail trader Tammy Chambless has been very forthcoming in sharing how she trades MEIC.

Thank you John. I am still trying to clarify one part. If your % wins are 40%, how do you make money? I see you mention winners are 2.2 times more profitable. But if you get equal premium on both sides, then how can winners be 2.2 time smore profitable?

Is this with tightening stops? Or is there something else you do?

Hi Diamond,

The profitability of a specific strategy can be measured by expectancy.

The formula for expectancy is the following:

Expectancy = (win rate % X size of the average win) – (loss rate % X size of the average loss).

So let’s say the average win is 220 dollars and the average loss is 100 dollars. That reflects the proportion in my trading. Let’s also say we have a win rate of 40% and a loss rate of 60 %.

That would give the following:

Expectancy = (0.4 X 220) – (0.6 X 100) = 88 – 60 = 28 dollars

With these numbers, you would make 28 dollars per trade on average – even though 60% of the trades are losers.

In other words: The profitability of a strategy never depends only on the win rate. You always also need to calculate the average sizes of wins and losses of the strategy.

yes..the problem is your average loss should be equal to your average win.. since you are getting stopped at your collected premium (which is your average win) thats why expectancy ends up being negative..

Hi Anders!

I want to research this. It seems to me that the intraday volatility has been higher in 2024 than before, but I have not had time to study if this is, in fact, the case. In my own trading, the big change that has affected the results negatively with this strategy is that the occurrences of double stop-losses is higher than in previous years.

There are quite a few trades that end around zero – or breakeven. I count them as profit if they are positive, even if it is only one dollar in profit, and likewise as loss if they are negative.

[…] have also traded it for a few months as a supplement to my bread-and-butter strategy 0DTE Breakeven Iron Condor. My results are at the same level as […]

[…] is a market-neutral 0DTE Iron Condor strategy that is very similar to my own 0DTE Breakeven Iron Condor strategy. There are many versions of the strategy, but the main rule is to sell multiple iron […]

[…] is my bread-and-butter strategy: 0DTE Breakeven Iron Condor. But it is not only mine. Retail trader Davíð Berndsen from Iceland has also had great […]

Did you consider checking the VIX levels compared with your daily returns and avoid trading when the VIX levels show correlations with your past losses?

Nicola: I have not done it systematically. But I did a small study on this a couple of years ago, and did not find a clear correlation between the VIX levels and my returns. I think it is rather the size of the intra-day moves that affects it – and those are very hard to predict.

[…] main strategy is MEIC (Multiple Entries Iron Condors), which resembles my bread-and-butter strategy 0DTE Breakeven Iron Condors. She also trades METF (Multiple Entries Trend Following). Learn more about METF in this […]

Very impressed with your approach and sharing all of this so transparently many thanks John. I am still not sure 0DTE is for me the gamma risk gives me jitters every time I try it out, with worst case scenario’s we all think of things like war these days but it could be far more mundane like if there is some broker outage (it happened very recently, with Tradier). But you (& Tammy and others) have convinced me that this can only work when you approach it systematically and( some variant of) your rules based approach, allowing the probabilities to come to expression. The flip side to all the worst case scenario talk is that this strategy should work in any market, probably even better in a bear market (?). Great stuff!

Thank you very much for your kind words, Tony! As I explain in the article, disciplined risk management is crucial for this strategy. By the way: Did you see our video interview with the Icelandic retail trader David Berndsen about the same strategy? https://www.thetaprofits.com/0dte-iron-condor-a-consistently-profitable-stratey/

Question, have you ever tried adjusting the stop loss further out when you see it’s coming close to being stopped, and opening another spread to hedge.

Asking because if you’re going to open another IC anyway, why not put on a higher stop loss when it’s close to being tested and then also open another spread on the other side at the same time.

This way if the market stays neutral there, everything will be a win. If it’s directional, it will stop them out as if they did if you didn’t manually adjust.

I have to review all of your material again (Blog, YouTube, Reddit, etc.) but for now, a quick question …

Do you set Profit Targets? Or do you just continue to tighten stops until they are hit?

I know you trade more discretionary than mechanically, but I’d like to attempt building an Option Alpha bot that is conceptually similar, if not exaclty the same.

I do have time to trade manually, but as a retired software developer I would love to create a bot. 🙂

No, I don’t set profit targets with this strategy beyond closing the shorts when they reach 5 cents in value. And I do tightened stop losses to some extent. Let me know how it goes with your Option Alpha bot!

Hi John, I happened to watch your video with David, it really opens my eyes on 0dte iron condor strategy – very impressive!

I have 2 questions

1. From https://optionalpha.com/blog/0dte, market neutral iron butterfly has a better risk-reward ratio and it generally generate profits faster than IC – which means a shorter time exposure to the market. Have you tried butterfly or any ideas to apply similar idea to butterfly?

2. When you say you would risk 1-2% of total position. Are you comparing the worst case situations at max loss or the double stop loss loss?

Hi Yi,

Thank you for your kind words!

1. I did try a version of iron butterfly in for a period – actually I wrote about it on my old site: https://www.sandvand.net/2022/11/26/the-results-of-100-trades-with-the-1dte-high-delta-iron-condor-options-strategy/

I have not traded it for a long time, though, as I decided to focus mostly on the 0DTE Breakeven Iron Condor as my 0DTE strategy.

2. I am considering the scenario where I will have double stop losses on all trades. And yes, I know there is a chance it might be bigger than that with bad fills, so I always try to look at my total positions. Sometimes all my risk is on one side with all the positions – in that case, I will be more careful than if the risk is on both sides. Sometimes I will put on a put or call spread just to hedge the risk.

Hi John. The amount of trades you have put on your 0DTE Breakeven Iron Condor strategy is amazing. I first heard you talk about this strategy at that Signapore webinar in 2023 and I decided to wait to see if your success continued and sure enough it did! You are an amazing fellow and I think I might start trading this strategy now that you have given us so much statistics. But I am still curious how you get double stop losses? Is it because the stop loss limit order just does not get filled at your specific price in time? What would happen if you only did stop market orders?

Thank you very much for your kind words!

As for double stop losses, I wonder if we misunderstand each other.

For me double stop losses are when the stop loss is hit both on the call and the put side. That happens in a few percent of the trades.

But it seems like you are thinking of when both the stop-limit order and the stop market order on the same side are hit simultaneously. Than happens only on a handful trades each year, and most of the times I end up profiting from it. I am not exactly clear how this can happen, but as I understand there is a very small chance it will occur. It would typically be in very volatile situations. It is a small challenge, but in most cases so far I have not been hurt by it.

With the year winding down, I was hoping you could provide a 2024 performance recap for your 0DTE Breakeven Iron Condor strategy. I see there has been an increase in double stop-losses in the first half of 2024 and was wondering if that trend has continued, and the impact of overall profitablility.

On a side note, I know you are aware of Option Omege. They are moving beyond backtesting and just did an online demo of their new automated trading platform. Yes, Option Omega will now have bots! 🙂 … The demo can be viewed on YouTube: https://www.youtube.com/watch?v=1s6_gHXn884

Personally, I do have the luxury of time to watch the market and execute trades manually, but I’d like to use Option Omega’s new bots to automate as much of your strategy as possible. There will likely always be human discretion involved, but the bots can do most of the “grunt work” of entering and managing trades.

It has been a tougher year for the strategy, although it has still been profitable. For the year so far I have a Premium Capture Rate of 3.53% and an average net profit per trade of 0.18%. This is lower than the previous years. Especially the last half of the year has seen a low profit. What about your results?

A follow-up question. Do you have an Option Omega backtest (or backtests) that you can share that follow your strategy? Reviewing the backtest parameters would help me learn your process.

To be honest, I do not know. My concern would be the overnight risks, especially connected with the stop losses. I suspect the chance of getting bad fills on the stop losses would be bigger.

[…] (RTS), builds on the fundamentals of the breakeven iron condor trading style, such as my own 0DTE Breakeven Iron Condor´strategy or the more disciplined Multiple Entries Iron Condors (MEIC) advocated by Tammy […]

Thank you for this excellent content, especially for those of us looking for ways to reduce risk. Two questions for you:

1. With Dale’s recent experience with the busted trade, have you reconsidered stop losses on only the short legs? From my understanding, Dale’s losses were worse than max loss for his initial trade because he closed the legs individually rather than the whole spread as one.

2. Do you have any advice for how to modify this strategy, if needed at all, to compensate for the increased volatility (wider daily ranges) we have seen lately?

This is a tricky one. I have noticed that many recommend closing the whole position, and not only the shorts. I still set the stops only on the shorts, as I have found it generally beneficial. But I am very aware of Dale’s experience, and also interviewed him about it. But this was an extreme outlier, as far as I understand.

Thank you, John. I did watch your interview with Dale and some of the other video commentators about his experience, but I am a novice in my understanding of the situation. I suppose the only way to avoid outliers is not to trade (in fact, I had a stop loss on a spread hit for 3x my entered amount just today).

I am a bit confused, if your total premium is say $300. Do you set a stop loss of $300 on the short put and another stop loss of $300 on the short call? Or do you set stop losses on shorts of $150 each for a total of $300. Earlier in this article you mentioned you set stop losses only on the short put. So do you set a stop on the short call side ?Thanks for any help.

Hi … I’ve been testing your method in a practice account and have done a few live trades on my trading account. I notice that a lot of times one side of the position gets challenged almost immediately. So theoretically I’d be out for a small loss if I didn’t get a double stop. Is that to be expected?

Thanks John. Appreciate your insights, sharings, and the interviews. Can you help me understand the loss in your calculations? My understanding is this, 1/ 40% winners (say avg profits 300$) 2/ 9% double stop with average loss at 600$ 3/ 51% Breakevens with one-sided stops, but these should be ~0. so wouldt the expected value =40% * 300-9%*600? and some change from remaining 51% BE positions?

Hi there, my understanding is the double stops would lose approx ($300) in your example as the both sides would lose $300 each but the initial premium received from the entire IC would be netted against the ($600). Either way, the Strat appears to have Positive Expectancy assuming small change from the 51% BE post’s, just a much larger PE if my thesis is correct

Hi John. Thanks for the great videos on Breakeven 0DTE Iron Condors. They are truly enlightening. My question is related to losses which seem to be about 25% of trades… with breakeven trades being about 35% and the balance being winning trades. If the strategy is designed to exit the trade at breakeven, I don’t understand how 25% of the trades can be losers. Wouldn’t there just be winning trades and breakeven trades… except for the rare occasions when stops are blown through? Thx!

I have been back testing this on OO all weekend. Can’t get it to work. Do you see anything I did wrong? This is only one test of many, all are negative. Tried various fixed premium and deltas. https://optionomega.com/share/IYf5Mnrb0K8TPZCVdtRC

I suggest you reach out to Tammy Chambless or others in the Quantum Options Facebook group. She is much more experienced in backtesting and automation than I am. https://www.facebook.com/groups/1275721603022231

Your 0DTE iron condor work reminds me why risk management beats strategy selection – I’ve seen traders blow accounts chasing high win rates without respecting drawdown phases. I’ve been testing Ratio X Toolbox’s MLAI 2.0 EA for my prop firm challenge, and it’s the first tool I’ve found that actually enforces stress testing and respects daily loss limits instead of hoping you’ll follow them manually. After two challenges myself, automating that discipline has been the real edge. Have you considered automating any part of your condor management, or are you keeping the execution fully manual for that breakeven adjustment?

I have been planning to test automation, but haven’t gotten around to it yet. I know many other traders do it. I think my style is a bit more discretionary than most Breakeven Iron Condor traders, though.

Hi John, great strategy and great content! My question is: how do you estimate the “extra value” of the long leg ($30 in your example) once you place a stop loss on the short leg? I find this quite challenging. It would be great if you could give some examples with puts and calls—should there be a different approach?

This is a bit of touch and feel, which is why I frequently adjust my stops. My way of trading does require that you monitor your positions frequently. But I always start with the stop value of the spread, which should be similar to the full premium collected for the Iron Condor. Let’s say this is $200. Then I add the current value of the long, let’s say that is $70. Then I add a measure for how much I guess that value will increase if the market moves in that direction, and we get close to the stop. This is the “gut feeling” of the equation. But typically, I will start with $30. If so, the calculation will be $200 + $70+ $30 = $300. I will start with that, and then adjust from what I see in the options chain. Typically, the “gut feeling” element will be bigger on the put side than on the call side.

Question, have you ever tried adjusting the stop loss further out when you see it’s coming close to being stopped, and opening another spread to hedge. Asking because if you’re going to open another IC anyway, why not put on a higher stop loss when it’s close to being tested and then also open another spread on the other side at the same time. This way if the market stays neutral there, everything will be a win. If it’s directional, it will stop them out as if they did if you didn’t manually adjust.

Commissions would be an issue. But I think an even bigger challenge would be that the liquidity is lower than on SPX. I expect that slippage would be a problem.

Hello,

I do not quite understand your maths. You say its break even when one of you SL is reached. Does not make sense to me. Surely, if price goes in a straight line for one of the 2 SL, it is losing, not break even.

Thanks for all the work!

Thank you John. I am still trying to clarify one part. If your % wins are 40%, how do you make money? I see you mention winners are 2.2 times more profitable. But if you get equal premium on both sides, then how can winners be 2.2 time smore profitable?

Is this with tightening stops? Or is there something else you do?

Hi Diamond,

The profitability of a specific strategy can be measured by expectancy.

The formula for expectancy is the following:

Expectancy = (win rate % X size of the average win) – (loss rate % X size of the average loss).

So let’s say the average win is 220 dollars and the average loss is 100 dollars. That reflects the proportion in my trading. Let’s also say we have a win rate of 40% and a loss rate of 60 %.

That would give the following:

Expectancy = (0.4 X 220) – (0.6 X 100) = 88 – 60 = 28 dollars

With these numbers, you would make 28 dollars per trade on average – even though 60% of the trades are losers.

In other words: The profitability of a strategy never depends only on the win rate. You always also need to calculate the average sizes of wins and losses of the strategy.

yes..the problem is your average loss should be equal to your average win.. since you are getting stopped at your collected premium (which is your average win) thats why expectancy ends up being negative..

Stop loss is separate for each side. So if only one side is triggered loss is much lower

Great write-up.

Could the answer to why the strategy has been less successful in 2024 be higher short-term volatility in the market overall?

Regards, Anders.

Hi Anders!

I want to research this. It seems to me that the intraday volatility has been higher in 2024 than before, but I have not had time to study if this is, in fact, the case. In my own trading, the big change that has affected the results negatively with this strategy is that the occurrences of double stop-losses is higher than in previous years.

John Einar

Thanks John, Are you counting the BE trades as losers? having trouble seeing your average loss calculations

There are quite a few trades that end around zero – or breakeven. I count them as profit if they are positive, even if it is only one dollar in profit, and likewise as loss if they are negative.

[…] have also traded it for a few months as a supplement to my bread-and-butter strategy 0DTE Breakeven Iron Condor. My results are at the same level as […]

[…] is a market-neutral 0DTE Iron Condor strategy that is very similar to my own 0DTE Breakeven Iron Condor strategy. There are many versions of the strategy, but the main rule is to sell multiple iron […]

[…] is my bread-and-butter strategy: 0DTE Breakeven Iron Condor. But it is not only mine. Retail trader Davíð Berndsen from Iceland has also had great […]

Did you consider checking the VIX levels compared with your daily returns and avoid trading when the VIX levels show correlations with your past losses?

Nicola: I have not done it systematically. But I did a small study on this a couple of years ago, and did not find a clear correlation between the VIX levels and my returns. I think it is rather the size of the intra-day moves that affects it – and those are very hard to predict.

Thank you for this info, I am curious how much the commissions cost, if you could share it would be helpful thank you!

Hi John,

I suppose a better way of asking would be is your results on the graphs after commissions or before? Thanks

These results are the net profits, meaning after commissions.

John Einar

Great thank you sir!

[…] main strategy is MEIC (Multiple Entries Iron Condors), which resembles my bread-and-butter strategy 0DTE Breakeven Iron Condors. She also trades METF (Multiple Entries Trend Following). Learn more about METF in this […]

Very impressed with your approach and sharing all of this so transparently many thanks John. I am still not sure 0DTE is for me the gamma risk gives me jitters every time I try it out, with worst case scenario’s we all think of things like war these days but it could be far more mundane like if there is some broker outage (it happened very recently, with Tradier). But you (& Tammy and others) have convinced me that this can only work when you approach it systematically and( some variant of) your rules based approach, allowing the probabilities to come to expression. The flip side to all the worst case scenario talk is that this strategy should work in any market, probably even better in a bear market (?). Great stuff!

Thank you very much for your kind words, Tony! As I explain in the article, disciplined risk management is crucial for this strategy. By the way: Did you see our video interview with the Icelandic retail trader David Berndsen about the same strategy? https://www.thetaprofits.com/0dte-iron-condor-a-consistently-profitable-stratey/

I did, and it was great just like your interview with Tammy, its great that you are sharing all of this, much appreciated!

Question, have you ever tried adjusting the stop loss further out when you see it’s coming close to being stopped, and opening another spread to hedge.

Asking because if you’re going to open another IC anyway, why not put on a higher stop loss when it’s close to being tested and then also open another spread on the other side at the same time.

This way if the market stays neutral there, everything will be a win. If it’s directional, it will stop them out as if they did if you didn’t manually adjust.

John,

Love the concept, the write up, and the video!

You mentioned a desire to get into backtesting. I would suggest OptionOmega.com. (I am not affiliated. Just a fan, and customer).

They also have an ‘Academy’. Tammy has already created a class. I’m sure the staff from Option Omega would love to hear from you.

… Bill

Thank you, Bill!

Yes, I know Option Omega – and plan to become a customer soon 🙂

By the way: Did you watch my interview with Tammy Chambless about backtesting?

https://www.thetaprofits.com/backtesting-options-strategies-with-tammy-chambless/

Thanks for you feedback! I love it!

John Einar

Hi John,

I have to review all of your material again (Blog, YouTube, Reddit, etc.) but for now, a quick question …

Do you set Profit Targets? Or do you just continue to tighten stops until they are hit?

I know you trade more discretionary than mechanically, but I’d like to attempt building an Option Alpha bot that is conceptually similar, if not exaclty the same.

I do have time to trade manually, but as a retired software developer I would love to create a bot. 🙂

Thanks … Bill

No, I don’t set profit targets with this strategy beyond closing the shorts when they reach 5 cents in value. And I do tightened stop losses to some extent. Let me know how it goes with your Option Alpha bot!

Hi John, I happened to watch your video with David, it really opens my eyes on 0dte iron condor strategy – very impressive!

I have 2 questions

1. From https://optionalpha.com/blog/0dte, market neutral iron butterfly has a better risk-reward ratio and it generally generate profits faster than IC – which means a shorter time exposure to the market. Have you tried butterfly or any ideas to apply similar idea to butterfly?

2. When you say you would risk 1-2% of total position. Are you comparing the worst case situations at max loss or the double stop loss loss?

Thanks!

Hi Yi,

Thank you for your kind words!

1. I did try a version of iron butterfly in for a period – actually I wrote about it on my old site: https://www.sandvand.net/2022/11/26/the-results-of-100-trades-with-the-1dte-high-delta-iron-condor-options-strategy/

I have not traded it for a long time, though, as I decided to focus mostly on the 0DTE Breakeven Iron Condor as my 0DTE strategy.

2. I am considering the scenario where I will have double stop losses on all trades. And yes, I know there is a chance it might be bigger than that with bad fills, so I always try to look at my total positions. Sometimes all my risk is on one side with all the positions – in that case, I will be more careful than if the risk is on both sides. Sometimes I will put on a put or call spread just to hedge the risk.

Hi John. The amount of trades you have put on your 0DTE Breakeven Iron Condor strategy is amazing. I first heard you talk about this strategy at that Signapore webinar in 2023 and I decided to wait to see if your success continued and sure enough it did! You are an amazing fellow and I think I might start trading this strategy now that you have given us so much statistics. But I am still curious how you get double stop losses? Is it because the stop loss limit order just does not get filled at your specific price in time? What would happen if you only did stop market orders?

Thank you very much for your kind words!

As for double stop losses, I wonder if we misunderstand each other.

For me double stop losses are when the stop loss is hit both on the call and the put side. That happens in a few percent of the trades.

But it seems like you are thinking of when both the stop-limit order and the stop market order on the same side are hit simultaneously. Than happens only on a handful trades each year, and most of the times I end up profiting from it. I am not exactly clear how this can happen, but as I understand there is a very small chance it will occur. It would typically be in very volatile situations. It is a small challenge, but in most cases so far I have not been hurt by it.

Hello John,

With the year winding down, I was hoping you could provide a 2024 performance recap for your 0DTE Breakeven Iron Condor strategy. I see there has been an increase in double stop-losses in the first half of 2024 and was wondering if that trend has continued, and the impact of overall profitablility.

On a side note, I know you are aware of Option Omege. They are moving beyond backtesting and just did an online demo of their new automated trading platform. Yes, Option Omega will now have bots! 🙂 … The demo can be viewed on YouTube: https://www.youtube.com/watch?v=1s6_gHXn884

Personally, I do have the luxury of time to watch the market and execute trades manually, but I’d like to use Option Omega’s new bots to automate as much of your strategy as possible. There will likely always be human discretion involved, but the bots can do most of the “grunt work” of entering and managing trades.

Thank you … Bill

It has been a tougher year for the strategy, although it has still been profitable. For the year so far I have a Premium Capture Rate of 3.53% and an average net profit per trade of 0.18%. This is lower than the previous years. Especially the last half of the year has seen a low profit. What about your results?

Hello John,

A follow-up question. Do you have an Option Omega backtest (or backtests) that you can share that follow your strategy? Reviewing the backtest parameters would help me learn your process.

Thanks again … Bill

I am sorry, I have not run a backtest on it.

[…] 0DTE Breakeven Iron Condor – my main strategy – represented 66.9% of my realized profits. […]

John,

Can this strategy work with 7DTE or longer trades?

To be honest, I do not know. My concern would be the overnight risks, especially connected with the stop losses. I suspect the chance of getting bad fills on the stop losses would be bigger.

[…] (RTS), builds on the fundamentals of the breakeven iron condor trading style, such as my own 0DTE Breakeven Iron Condor´strategy or the more disciplined Multiple Entries Iron Condors (MEIC) advocated by Tammy […]

Hello John

Are you still trading the breakeven iron condor in 2025?

Are the results consistent with the ones of the previous years?

Thank you

How would this strategy work with when trading 0DTE option on futures like /es? do you believe the results would be similar?

I honestly don’t know. I have never traded options on futures.

Hi, John,

Thank you for this excellent content, especially for those of us looking for ways to reduce risk. Two questions for you:

1. With Dale’s recent experience with the busted trade, have you reconsidered stop losses on only the short legs? From my understanding, Dale’s losses were worse than max loss for his initial trade because he closed the legs individually rather than the whole spread as one.

2. Do you have any advice for how to modify this strategy, if needed at all, to compensate for the increased volatility (wider daily ranges) we have seen lately?

Thank you again.

This is a tricky one. I have noticed that many recommend closing the whole position, and not only the shorts. I still set the stops only on the shorts, as I have found it generally beneficial. But I am very aware of Dale’s experience, and also interviewed him about it. But this was an extreme outlier, as far as I understand.

Thank you, John. I did watch your interview with Dale and some of the other video commentators about his experience, but I am a novice in my understanding of the situation. I suppose the only way to avoid outliers is not to trade (in fact, I had a stop loss on a spread hit for 3x my entered amount just today).

Can you elaborate why you aim for equal premium on both sides? Does that not put one of the sides on much higher delta than the other?

Hey when you enter the position for the day let’s say 2%. Once you have enter that full risk, you don’t add any more positions on afterwards?

I am a bit confused, if your total premium is say $300. Do you set a stop loss of $300 on the short put and another stop loss of $300 on the short call? Or do you set stop losses on shorts of $150 each for a total of $300. Earlier in this article you mentioned you set stop losses only on the short put. So do you set a stop on the short call side ?Thanks for any help.

Hi … I’ve been testing your method in a practice account and have done a few live trades on my trading account. I notice that a lot of times one side of the position gets challenged almost immediately. So theoretically I’d be out for a small loss if I didn’t get a double stop. Is that to be expected?

Thank you John for the great video!

May i ask for the fees?

THX Dieter

Thanks John. Appreciate your insights, sharings, and the interviews. Can you help me understand the loss in your calculations? My understanding is this, 1/ 40% winners (say avg profits 300$) 2/ 9% double stop with average loss at 600$ 3/ 51% Breakevens with one-sided stops, but these should be ~0. so wouldt the expected value =40% * 300-9%*600? and some change from remaining 51% BE positions?

Hi there, my understanding is the double stops would lose approx ($300) in your example as the both sides would lose $300 each but the initial premium received from the entire IC would be netted against the ($600). Either way, the Strat appears to have Positive Expectancy assuming small change from the 51% BE post’s, just a much larger PE if my thesis is correct

Hi John. Thanks for the great videos on Breakeven 0DTE Iron Condors. They are truly enlightening. My question is related to losses which seem to be about 25% of trades… with breakeven trades being about 35% and the balance being winning trades. If the strategy is designed to exit the trade at breakeven, I don’t understand how 25% of the trades can be losers. Wouldn’t there just be winning trades and breakeven trades… except for the rare occasions when stops are blown through? Thx!

Jon,

Thanks for all the information you shared!

Thank you!

I have been back testing this on OO all weekend. Can’t get it to work. Do you see anything I did wrong? This is only one test of many, all are negative. Tried various fixed premium and deltas. https://optionomega.com/share/IYf5Mnrb0K8TPZCVdtRC

I suggest you reach out to Tammy Chambless or others in the Quantum Options Facebook group. She is much more experienced in backtesting and automation than I am. https://www.facebook.com/groups/1275721603022231

Your 0DTE iron condor work reminds me why risk management beats strategy selection – I’ve seen traders blow accounts chasing high win rates without respecting drawdown phases. I’ve been testing Ratio X Toolbox’s MLAI 2.0 EA for my prop firm challenge, and it’s the first tool I’ve found that actually enforces stress testing and respects daily loss limits instead of hoping you’ll follow them manually. After two challenges myself, automating that discipline has been the real edge. Have you considered automating any part of your condor management, or are you keeping the execution fully manual for that breakeven adjustment?

I have been planning to test automation, but haven’t gotten around to it yet. I know many other traders do it. I think my style is a bit more discretionary than most Breakeven Iron Condor traders, though.

[…] John Einar Sandvand: 0DTE Breakeven Iron Condor […]

Hi John, great strategy and great content! My question is: how do you estimate the “extra value” of the long leg ($30 in your example) once you place a stop loss on the short leg? I find this quite challenging. It would be great if you could give some examples with puts and calls—should there be a different approach?

This is a bit of touch and feel, which is why I frequently adjust my stops. My way of trading does require that you monitor your positions frequently. But I always start with the stop value of the spread, which should be similar to the full premium collected for the Iron Condor. Let’s say this is $200. Then I add the current value of the long, let’s say that is $70. Then I add a measure for how much I guess that value will increase if the market moves in that direction, and we get close to the stop. This is the “gut feeling” of the equation. But typically, I will start with $30. If so, the calculation will be $200 + $70+ $30 = $300. I will start with that, and then adjust from what I see in the options chain. Typically, the “gut feeling” element will be bigger on the put side than on the call side.

Question, have you ever tried adjusting the stop loss further out when you see it’s coming close to being stopped, and opening another spread to hedge. Asking because if you’re going to open another IC anyway, why not put on a higher stop loss when it’s close to being tested and then also open another spread on the other side at the same time. This way if the market stays neutral there, everything will be a win. If it’s directional, it will stop them out as if they did if you didn’t manually adjust.

[…] John Einar Sandvand: 0DTE Breakeven Iron Condor […]

[…] starting point for the discussion is the 0DTE Breakeven Iron Condor strategy, also known as Multiple Entries Iron Condors […]

Would this work on XSP too or would the commissions eat too much of it?

Commissions would be an issue. But I think an even bigger challenge would be that the liquidity is lower than on SPX. I expect that slippage would be a problem.

Hi John, thanks for the great webinar.

I have a question. Do you open all positions s at the same strikes or each position targets 10-15 delta open?

Hello,

I do not quite understand your maths. You say its break even when one of you SL is reached. Does not make sense to me. Surely, if price goes in a straight line for one of the 2 SL, it is losing, not break even.

Thanks for all the work!

CS